From New World ERP’s first misconfigured day in July 2009 to the Auditor of State

ordering the budget-checking override permissions locked down in October 2025 —

the receipts have been here the entire time.

{kind=link}

.

Executive Summary

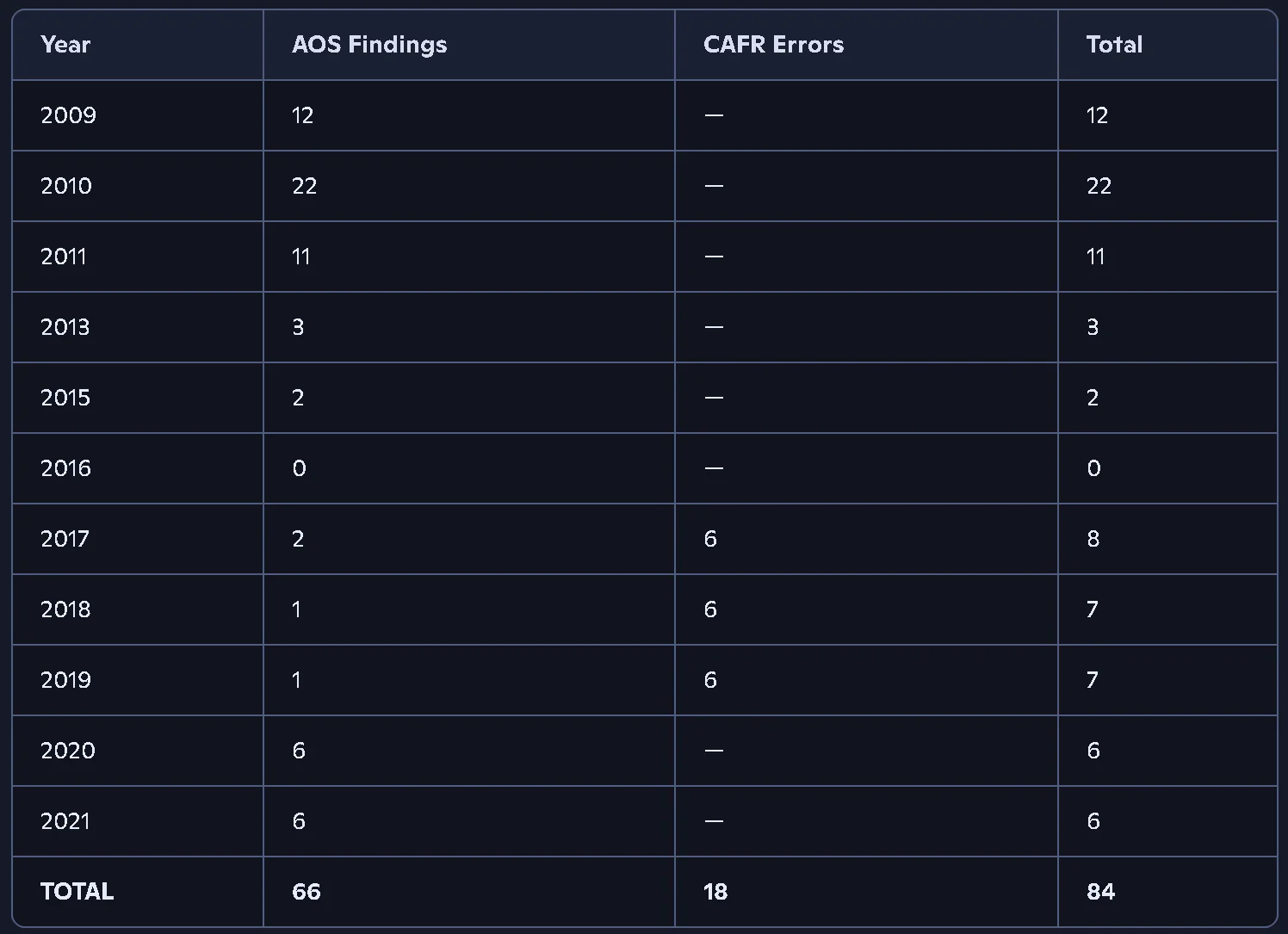

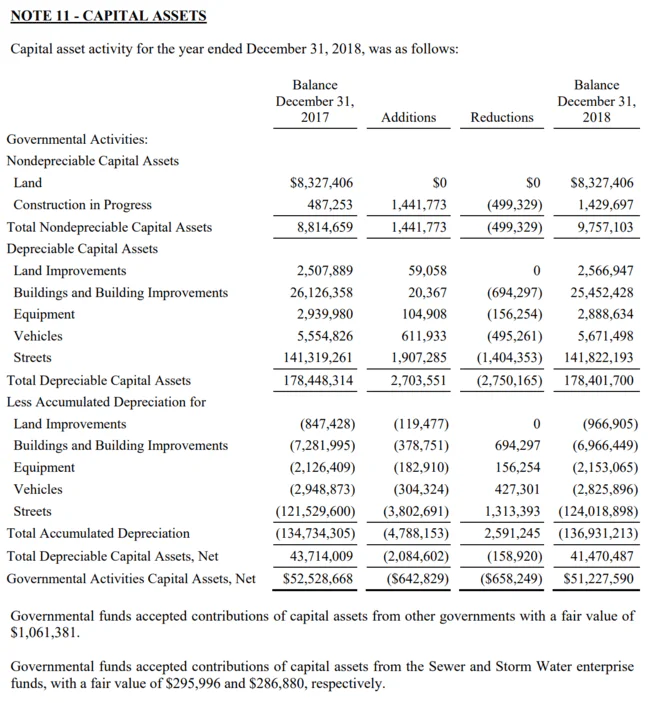

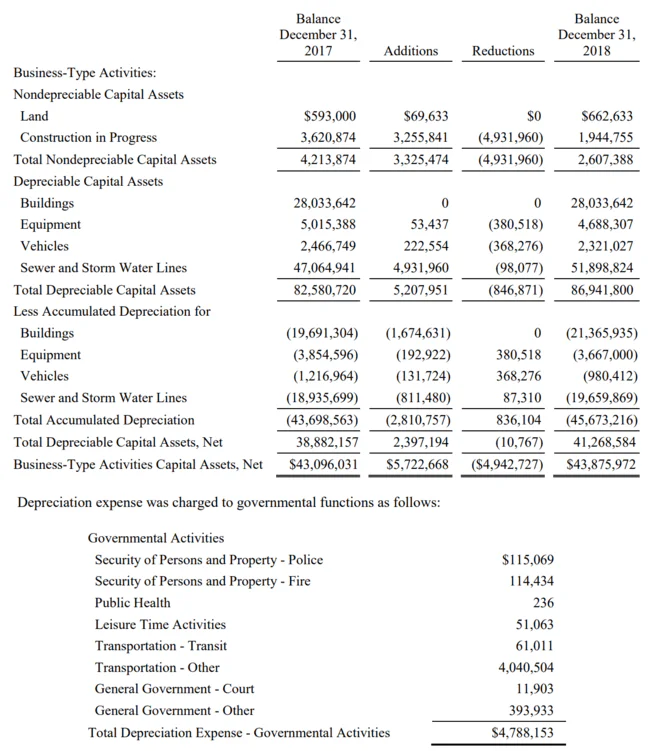

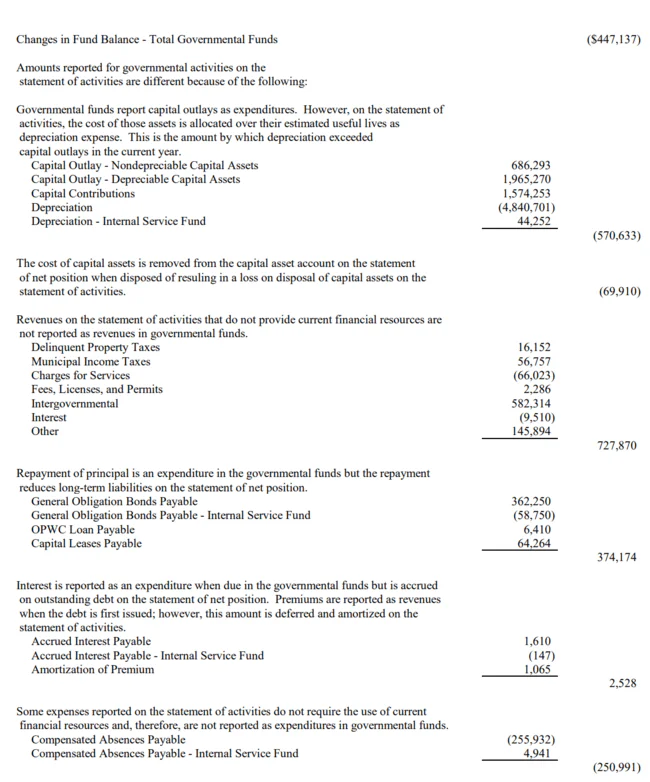

The City of Marion, Ohio, implemented the New World ERP accounting system in July 2009. From the moment it went live, the Ohio Auditor of State began documenting a cascade of internal control failures, budget overrides, unreconciled accounts, and missing money. Across seven formal audit cycles spanning 2009 through 2021, state auditors issued a combined 66 formal findings—including material weaknesses, material noncompliance citations, significant deficiencies, and findings for recovery totaling hundreds of thousands of dollars. During the three-year gap between audits (2017–2019), the City produced its own financial reports containing 18 additional categories of financial reporting errors—including a $5,128,212 unexplained discrepancy between two expenditure totals in the same report, internal income tax revenue contradictions, fund balance irregularities, and capital asset inventory inconsistencies.

Gasoline in the fire such as shared passwords, inappropriate elevated permissions to the New World system with no business justification, lack of segregation of duties, physical security breaches, and other grave IT failures greatly increased the explosion and damage to the City of Marion you are about to read. This is the undeniable failure of the New World system under the Schertzer administration, making everything in this report draw to one conclusion: this is the predictable outcome to a lack of financial and IT controls finally exposed and addressed under the Collins administration.

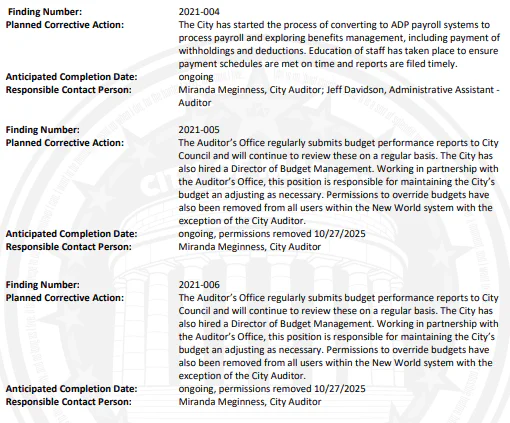

The pattern is unmistakable: the system’s controls were never properly configured, budget override permissions were left wide open to all users, bank reconciliations went months or years without completion, and hundreds of thousands of dollars were misdirected, misallocated, or simply vanished. It was not until October 27, 2025—more than 16 years after implementation—that the City finally removed budget-checking override permissions from all New World users except the City Auditor.

Key dollar figures in the paper trail:

- $543,079 — Unreconciled bank-to-book variance, December 31, 2021

- $314,347 — Unreconciled bank-to-book variance, December 31, 2020

- $1,184,754 — Federal withholdings erroneously sent to Ohio Dept. of Taxation instead of IRS

- $279,036.80 — Total withholding penalties across multiple agencies (plus $146,169.38 abated)

- $154,399 — Finding for Recovery against City Auditor Robert Landon III

- $34,276 — Utility payments stolen by Brenda Nwosu (2011–2014)

- $22,500 — W-2 late-filing penalties, Finding for Recovery against Kelly Carr

- $5,128,212 — Unexplained gap between fund-level and government-wide expenditure totals (2018 report)

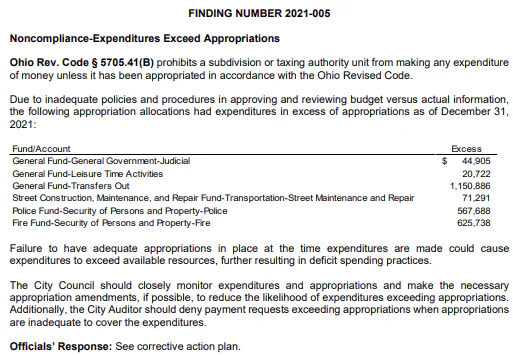

- $1,150,886 — General Fund Transfers Out exceeding appropriations (2021)

- $625,738 — Fire Fund exceeding appropriations (2021)

- $567,688 — Police Fund exceeding appropriations (2021)

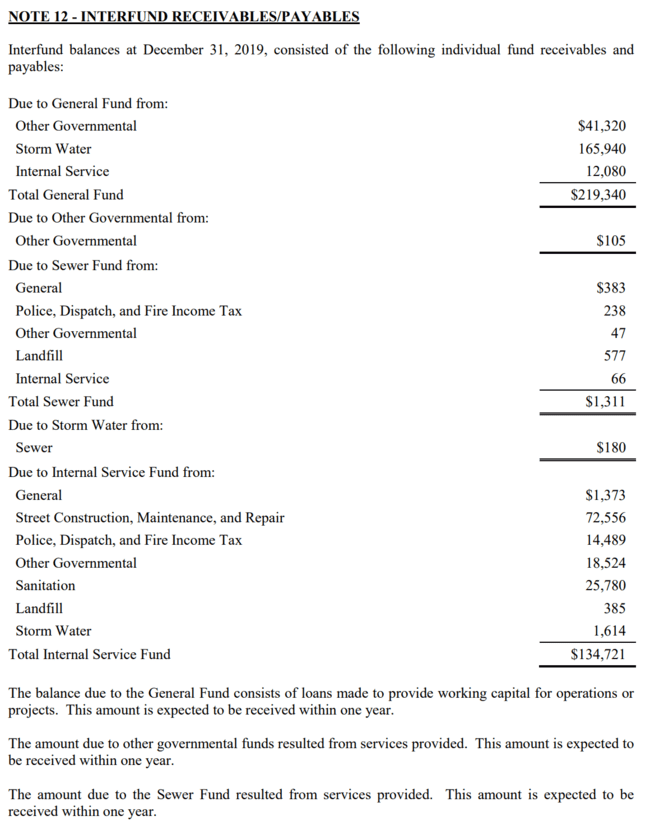

- $89,411 — Cross-fund payment, Sewer from Landfill Fund (2010)

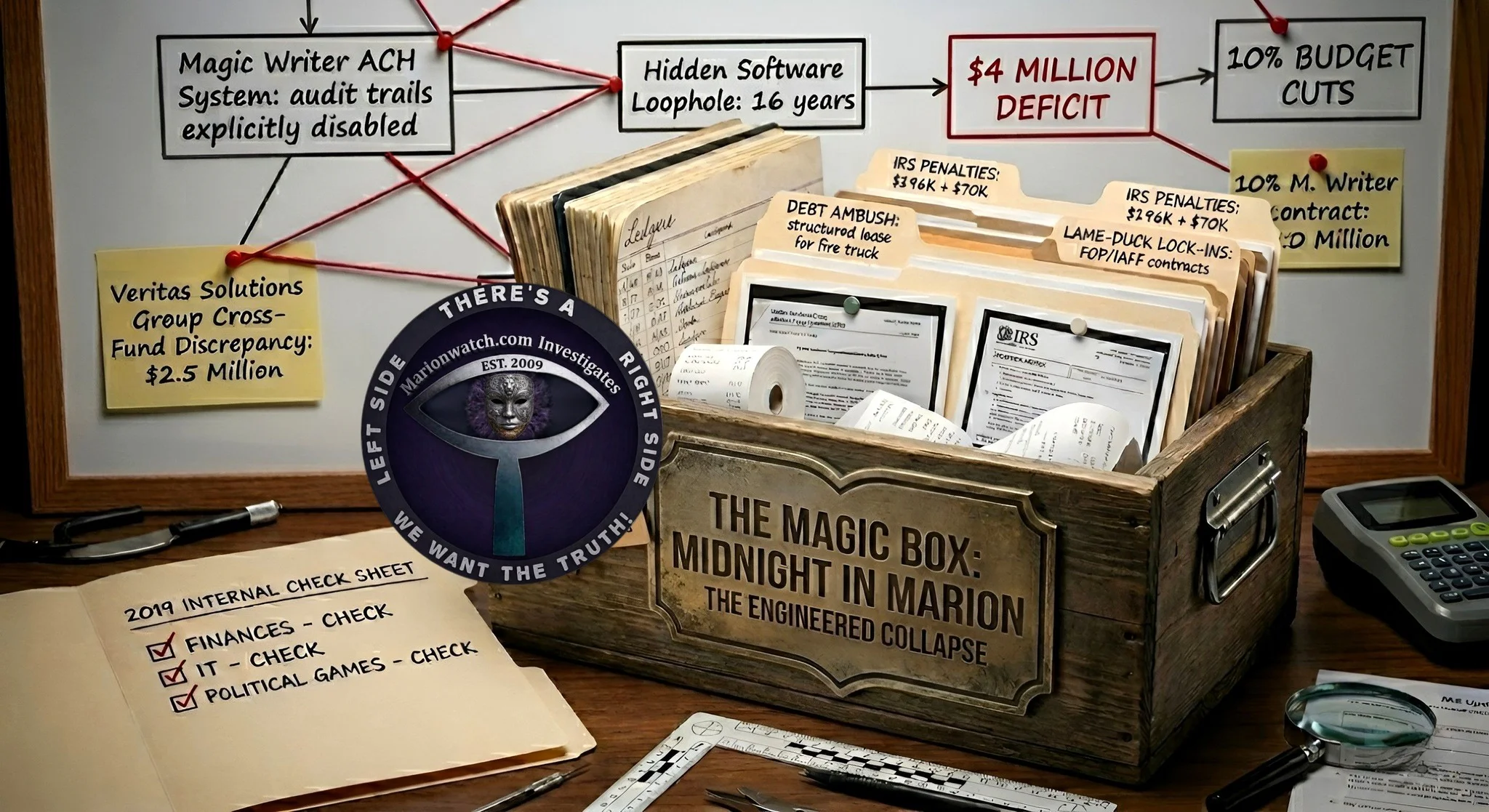

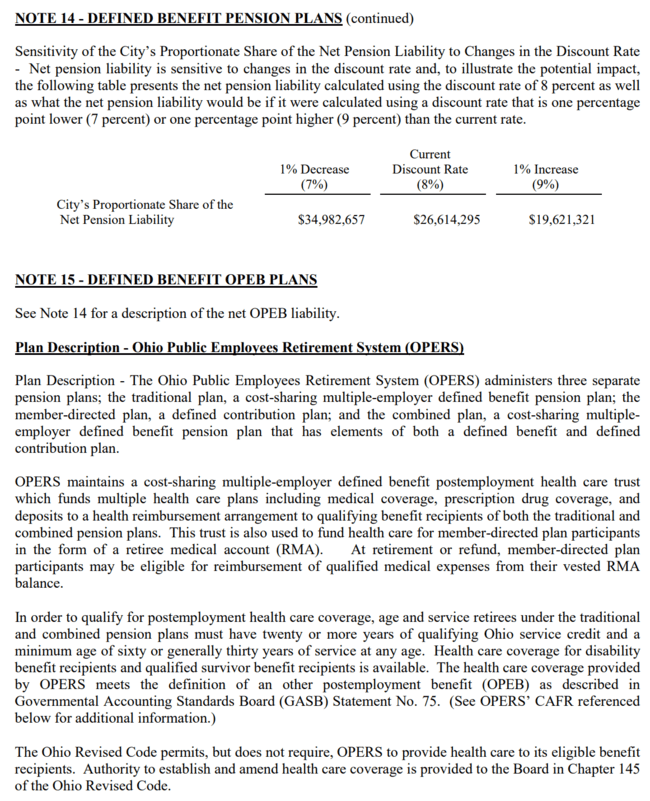

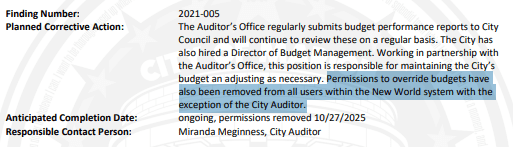

The most critical revelation: the 2021 audit’s corrective action plans explicitly name the New World ERP system for the first time, and state that budget override permissions were finally removed from all users except the City Auditor on October 27, 2025—more than 16 years after implementation.

Seventy-eight formal Auditor of State findings. Eighteen categories of financial reporting errors in City-produced reports. Ten reporting periods spanning seventeen years. One ERP system with its controls left wide open from the day it was installed.

The Auditor of State documented it all. The findings were public. The corrective action plans were filed. And for sixteen years, three months, and twenty-seven days, the budget-checking override permissions in the New World ERP system remained assigned to every user with spending authority.

The receipts have been here the entire time. This could have been stopped many years ago, had someone just listened. This is the reason why Marion Watch and many officials are demanding a full forensic IT audit, which is a non-negotiable standard when issues of this magnitude are present.

Methods and Sources

This investigation is rooted exclusively in primary source documentation. Every finding, discrepancy, and system failure detailed in this report is derived from official Auditor of State reports, the City of Marion’s own self-produced financial statements, and verified public records obtained through formal requests.

Our analysis is governed by a strict adherence to global IT, legal, and financial industry standards, ensuring that every conclusion is anchored in established regulatory frameworks. This methodology is designed to provide a rigorous, objective assessment that meets the highest standards of professional accountability.

Regulatory and Professional Frameworks

Our findings are evaluated against the following benchmarks:

- Financial Reporting Standards: Benchmarking all municipal reporting against GASB (Governmental Accounting Standards Board) requirements and GFOA (Government Finance Officers Association) best practices for transparency and financial health.

- IT Governance & Cybersecurity: Evaluating system configurations and administrative controls against NIST (National Institute of Standards and Technology) and COBIT (Control Objectives for Information and Related Technologies) frameworks. This includes strict adherence to the Principle of Least Privilege (PoLP) and Segregation of Duties (SoD).

- Operational Integrity: Applying ITIL (Information Technology Infrastructure Library) standards to assess the City’s change management and service delivery, alongside AICPA Trust Services Criteria to evaluate the Processing Integrity of the General Ledger.

- Legal Compliance: Assessing all administrative and financial actions against the Ohio Revised Code (ORC) and federal 2 CFR 200 (Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards).

Technical Expertise and Consultation

To ensure the technical accuracy of this analysis, Marion Watch leveraged over 20 years of internal expertise in full-stack information technology infrastructure, complex systems administration, and regulatory compliance. Our methodology was further strengthened through extensive, multi-level consultation with a broad network of stakeholders, including:

- Current Municipal Leadership: Direct engagement and consultation with the Collins Administration and members of the Marion City Council to understand current operational status and active corrective measures.

- Historical and Regional Context: Consultations with past elected officials from Marion and surrounding jurisdictions to verify long-term administrative patterns and institutional memory.

- Global Professional Network: Collaboration with a network of certified professionals and subject matter experts from across the State of Ohio, several other U.S. states, and international experts in ERP governance, municipal finance, and investigative journalism.

Final Declaration of Objectivity

Our approach is strictly evidentiary: we provide no speculation and no inference beyond what the verified documents and system configurations support. We have meticulously analyzed the “digital fingerprints” left by sixteen years of administrative decisions. In the interest of public transparency and government accountability, we maintain that the facts are self-evident—the receipts speak for themselves.

The Complete Story: How New World ERP Failed Marion

In July 2009, the City of Marion, Ohio, flipped the switch on a new accounting system. New World ERP—an integrated, Windows-based financial management platform built for municipal government—replaced the City’s legacy systems and promised modern fund accounting, automated budget controls, streamlined purchasing workflows, and real-time financial reporting. It was supposed to make the City’s finances more transparent, more accurate, and more accountable.

It did none of those things.

From the very first audit cycle after go-live, the Ohio Auditor of State began documenting failures. Finding 2009-001—”Financial Monitoring”—noted that “the City did not have an effective control process established over the financial activity recorded on the City’s ledgers.” Officials with monitoring responsibilities had been given “limited training” on the new system. The City’s response was telling: “The City of Marion agrees that additional trainings will be beneficial.” It was the beginning of a pattern that would repeat for sixteen years—auditors identify a system-enabled failure, the City promises to do better, and nothing changes.

The bank reconciliations collapsed almost immediately. Finding 2009-002 documented that “the City’s monthly bank reconciliations have not been completed in a timely manner” since the new system was implemented. The City Auditor’s office and the City Treasurer were jointly performing reconciliations—destroying the Segregation of Duties that is the most basic internal control in government finance. The City’s defense: “The City of Marion recognizes when working within two systems there could be room for oversight. With the City of Marion now on one system, internal controls are tighter.”

They were not.

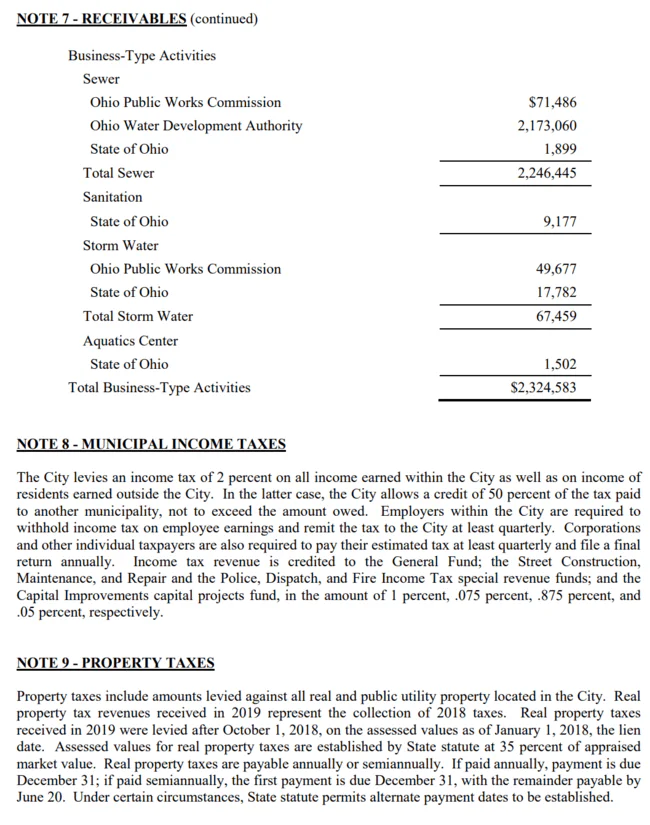

Income tax allocations were wrong from day one. The City has a 1% unvoted and 0.75% voted municipal income tax, with allocations governed by specific ordinances. Finding 2009-005 documented that “income tax receipts were not allocated in accordance with the above ordinances”—and that the beginning fund balances for 2009 were also incorrect because 2008 allocations had been wrong too. The New World system’s revenue distribution rules were never configured to match the ordinance requirements.

Purchase orders sailed through without approval. Finding 2009-007 found that 23% of expenditures had purchase orders that “were not reviewed and approved by the appropriate department supervisor.” The City blamed the transition: “During conversion from the old system to the new system, the old purchase orders were approved on paper by the supervisor. When the new system was implemented, these same purchase orders were re-entered into the new system and no approval was necessary.” In other words, the Purchasing module’s approval workflow was not configured to require approval for migrated purchase orders—a configuration choice that created a 23% bypass rate.

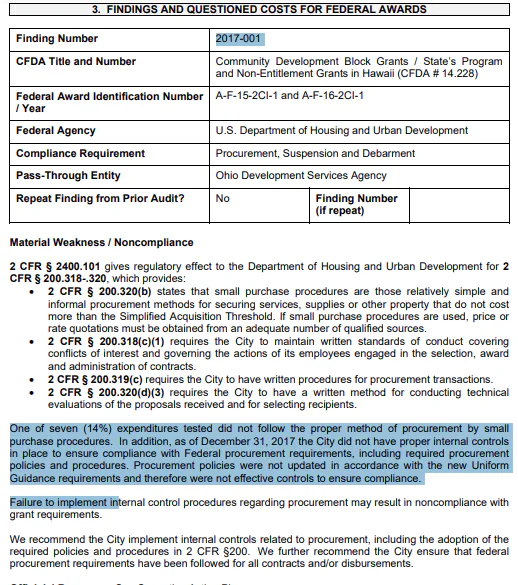

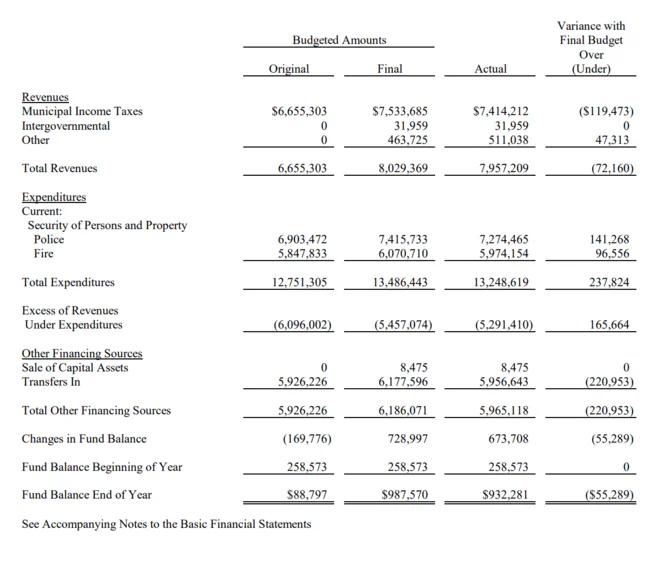

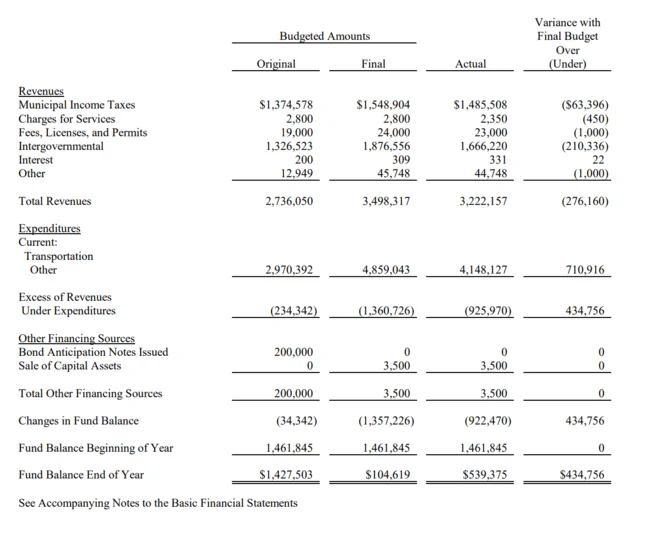

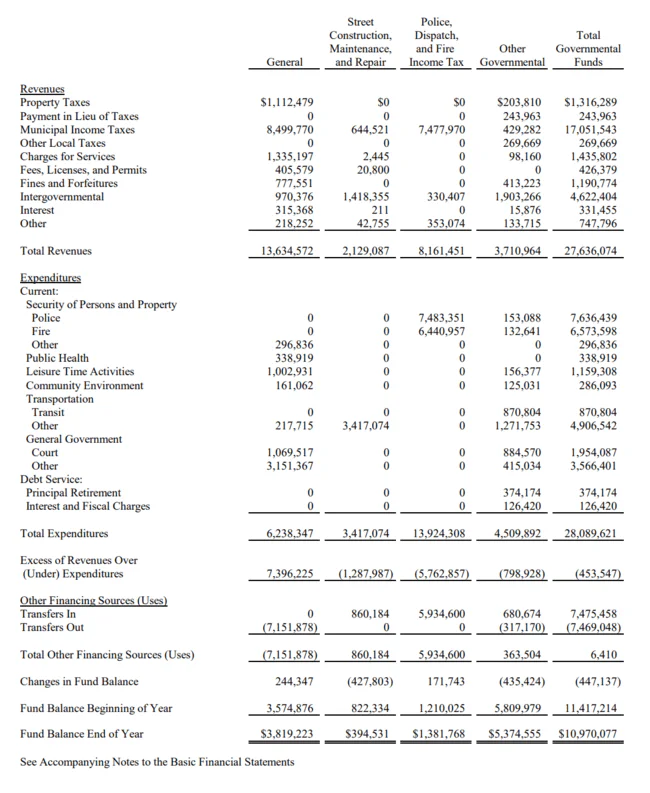

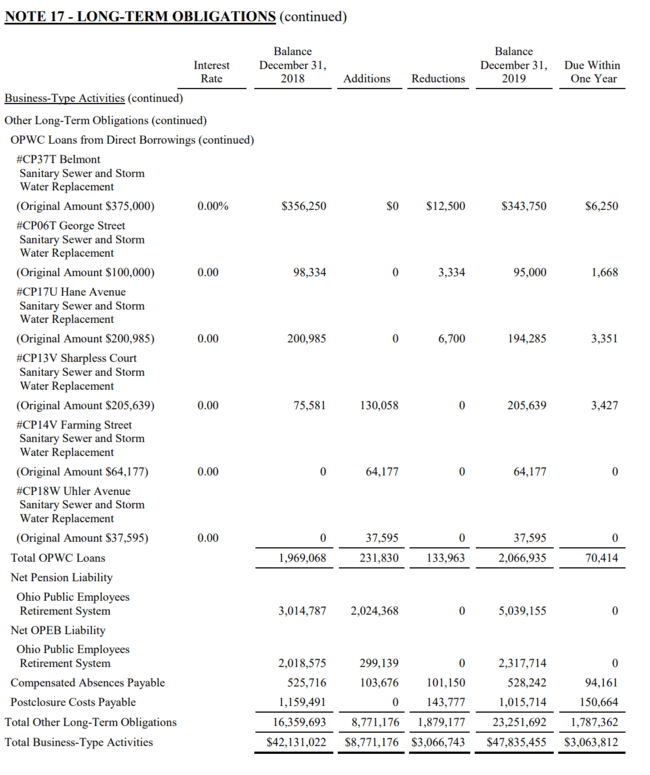

And then there were the budget overrides. Finding 2009-008 documented that “budgetary expenditures exceeded appropriations at the legal level of control materially.” This is the finding that would haunt Marion for the next sixteen years. New World’s Purchasing module includes a budget-checking feature that validates every transaction against appropriated amounts. It has a built-in override capability—a designed feature that allows authorized personnel to process emergency or extraordinary expenditures when budget-checking indicates insufficient appropriation. The key word is “authorized.” In Marion, override permissions were assigned to virtually every user in the system. Anyone with spending authority could bypass the budget ceiling. The system dutifully logged every override, but nobody was watching the logs.

By 2010, the problems had multiplied to 22 findings in a single audit (including findings 2010-015 through 2010-022). Negative fund balances appeared—the City paid $89,411 of Sewer Fund debt service from the Landfill Fund, a cross-fund payment that should have been blocked by the system. By 2011, the Auditor noted that the City had “suffered recurring losses from operations and has a net asset deficiency.” Federal program findings piled up—questioned costs in CDBG and Rural Transit grants, late single audit filings, improper cost allocations. The same finding categories repeated year after year: budget overrides, negative fund balances, investment procedure failures, and purchasing authorization bypasses.

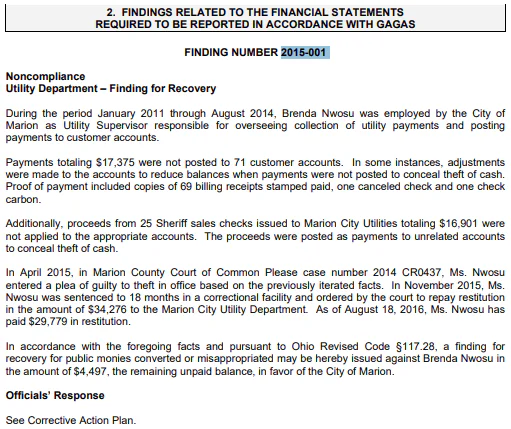

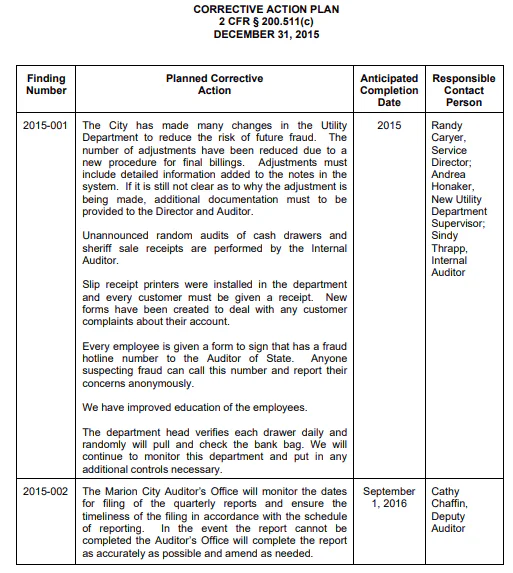

In 2015, the consequences turned criminal. Brenda Nwosu, Utility Supervisor from January 2011 through August 2014, embezzled $34,276 from utility payment collections. Payments totaling $17,375 were not posted to 71 customer accounts. “In some instances, adjustments were made to the accounts to reduce balances when payments were not posted to conceal theft of cash.” An additional $16,901 in Sheriff sale proceeds were redirected. The New World Utility Billing module’s controls failed to flag unposted payments, unauthorized account adjustments, or the redirection of Sheriff sale proceeds. Per GFOA standards, the person handling cash should never have the ability to adjust account balances—but in Marion’s system, they did.

2016 brought the only clean audit in the entire span—zero findings. It was an anomaly, not a turning point.

The findings kept coming.

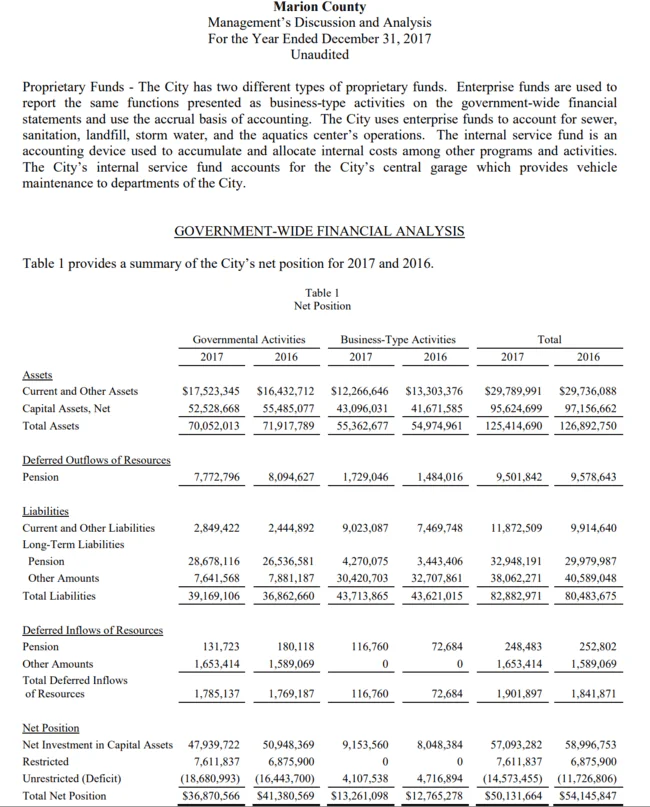

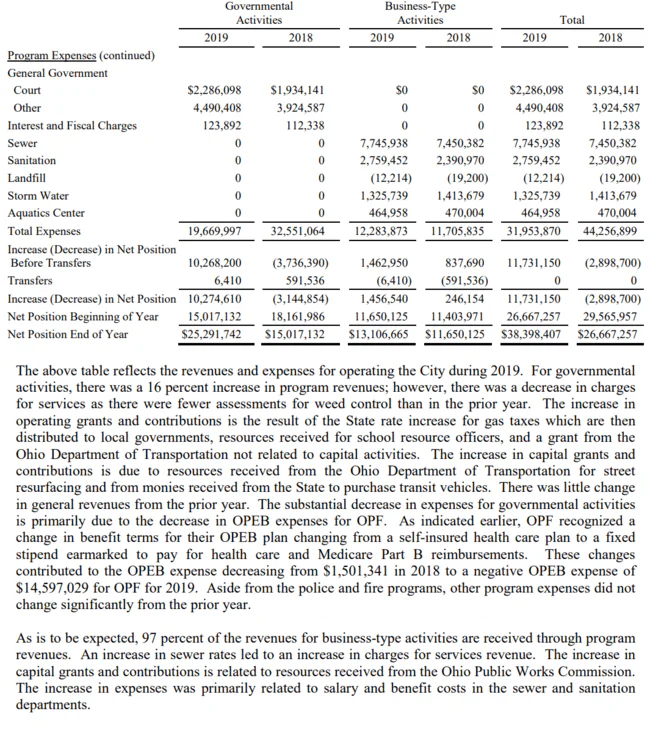

The City’s financial reports for 2017 through 2019 documented the same patterns the Auditor of State had flagged since 2009—and introduced new ones. The 2017 CAFR contained net position discrepancies in both governmental activities ($41,380,569) and business-type activities ($12,765,278), underreported property tax and income tax revenue, departmental expenditure inaccuracies across police ($6,854,807 underreported), fire, and public health, debt service calculation errors, and fund balance irregularities in the General Fund ($2,921,053).

The 2018 financial report was worse: a $5,128,212 unexplained gap between the fund-level expenditure total ($25,762,379) and the government-wide Statement of Activities ($30,890,591), a $42,019 internal variance in the City’s own municipal income tax figures, and an unexplained 28.8% collapse in transit ridership—from 167,680 riders to 119,457—that nobody analyzed.

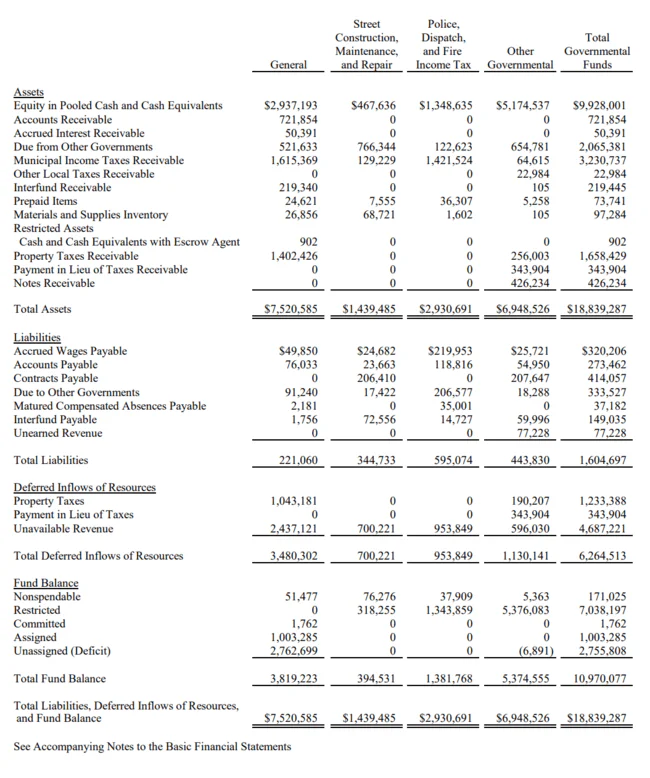

By 2019, the financial report showed fund balance classification inconsistencies, general obligation bond totals ($24,583,763) that did not reconcile with their own detailed breakdowns, income tax revenue contradictions between component sums and reported totals, and a police vehicle inventory that could not agree with itself—27 vehicles in one section, 30 in another. The same New World ERP system producing these reports was the same system that had been flagged for control failures since 2009—and every category of error traced back to the same uncorrected configuration deficiencies.

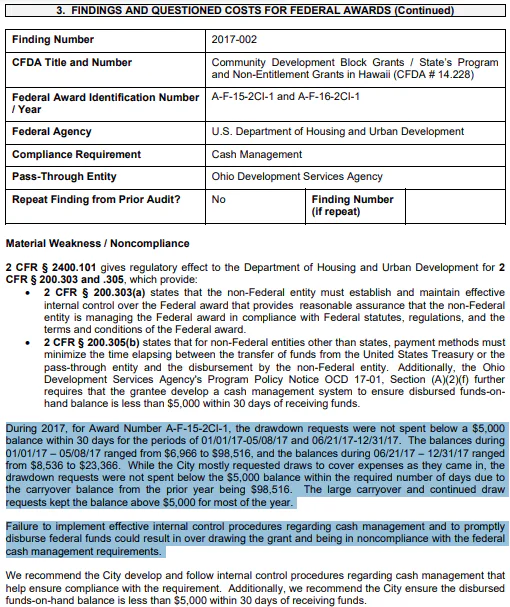

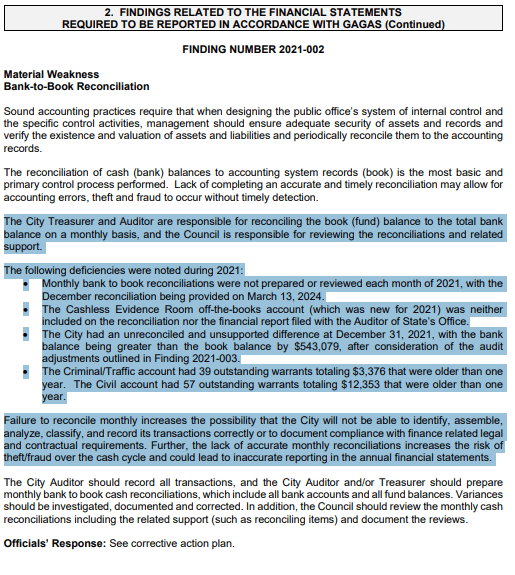

When the Auditor of State returned for the 2020 audit, the results were catastrophic. The bank reconciliation was off by $314,347—”with the book balance being greater than the bank balance due to the lack of monthly bank-to-book reconciliations and the complexity of the City’s accounting software (i.e. hybrid cash/accrual basis).” The Auditor explicitly cited the accounting software’s configuration as a contributing factor.

Worse: the City had erroneously remitted $1,184,754 in 3rd and 4th quarter 2020 federal tax withholdings to the Ohio Department of Taxation instead of the Internal Revenue Service. The error began in June 2020 and was not identified until January 2021—seven months of misdirected payments. Correcting payments of $1,184,754 were made to the IRS on February 9, 2021, but the City did not appropriate for these payments until November 8, 2021. The result: a Finding for Recovery of $154,399 in penalties and interest against City Auditor Robert Landon III and his bonding company. A separate Finding for Recovery of $22,500 was issued against former City Auditor Kelly Carr for penalties incurred when the 2018 W-2s were filed late.

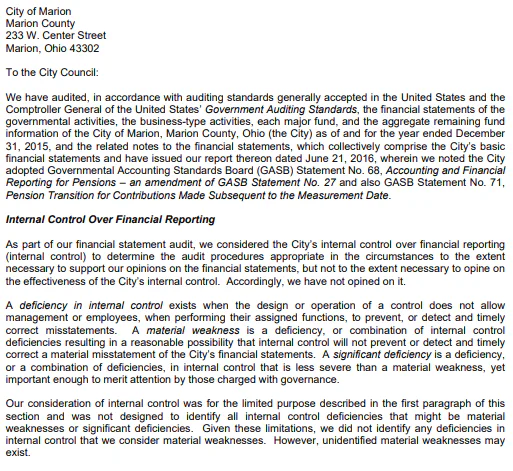

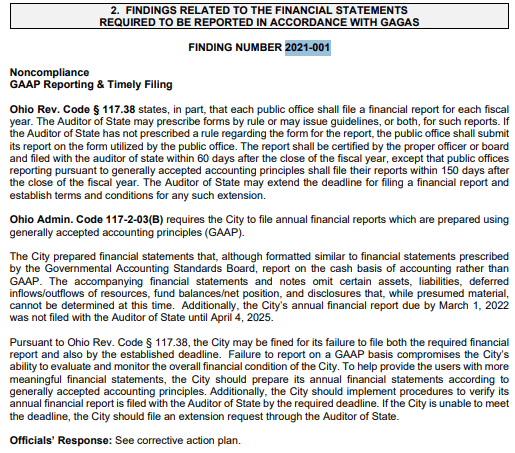

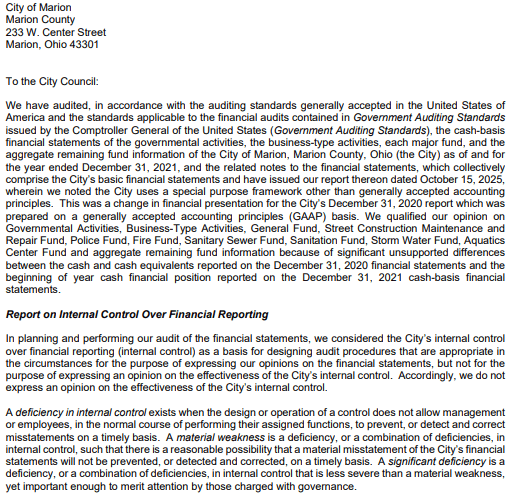

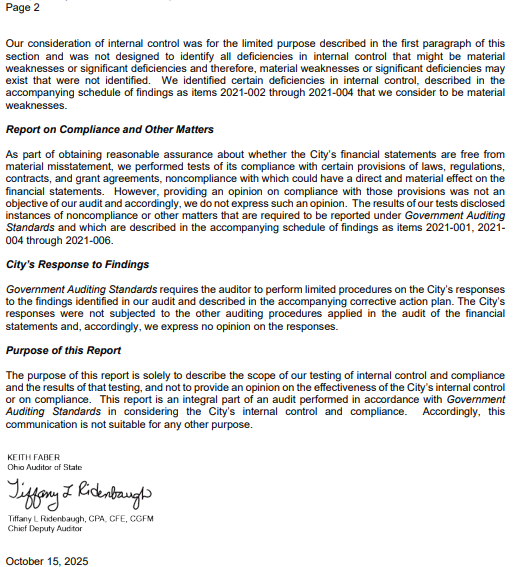

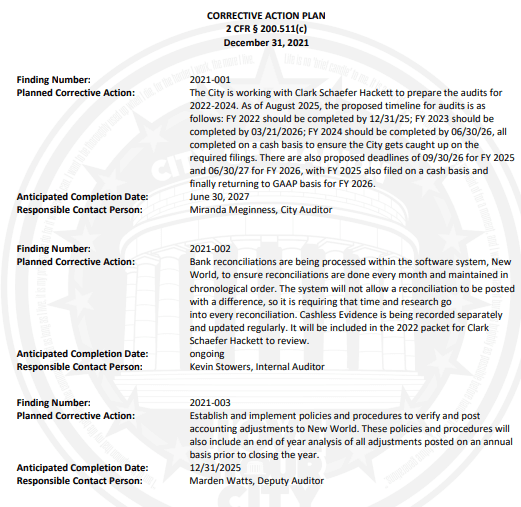

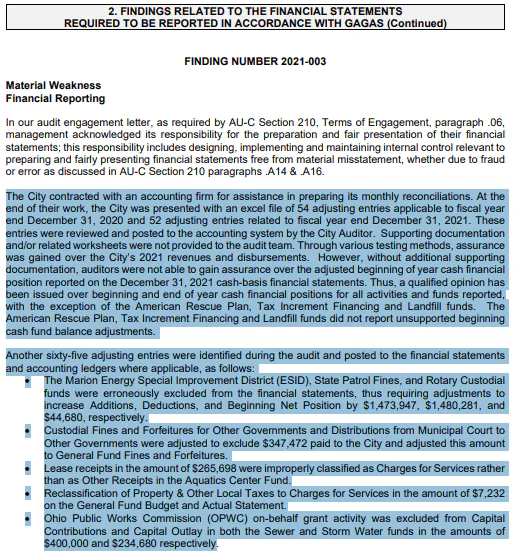

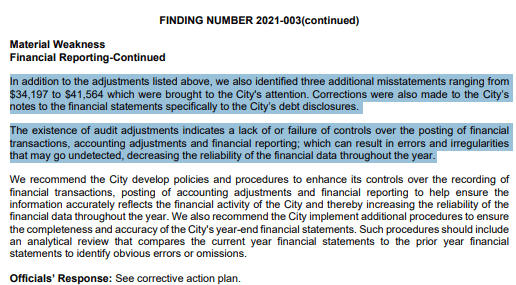

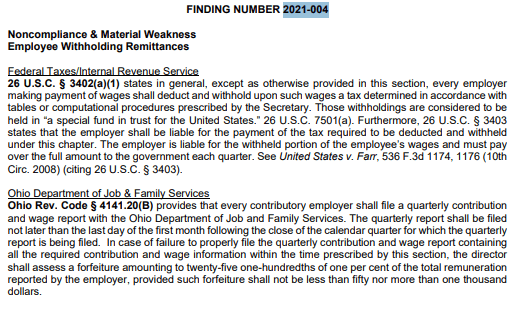

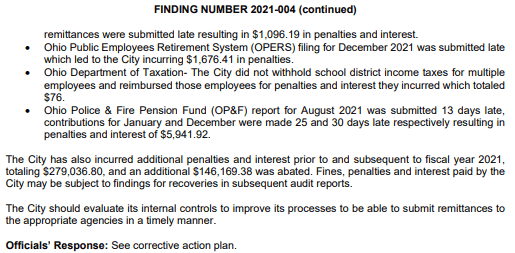

The 2021 audit—filed October 15, 2025, and certified for release November 13, 2025—brought the final reckoning. Qualified opinions were issued on most fund statements. A contracted accounting firm had to post 54 adjusting entries for fiscal year 2020 and 52 for fiscal year 2021, with 65 additional adjustments identified during the audit itself. The bank reconciliation showed an unreconciled difference of $543,079. Employee withholding remittances were late to the IRS, OPERS, OP&F, and the Ohio Department of Taxation, resulting in $279,036.80 in penalties plus an additional $146,169.38 that was abated.

And then came the corrective action plans—the first official documents in the entire 17-year record to name the New World system explicitly:

“Bank reconciliations are being processed within the software system, New World, to ensure reconciliations are done every month and maintained in chronological order. The system will not allow a reconciliation to be posted with a difference, so it is requiring that time and research go into every reconciliation.”

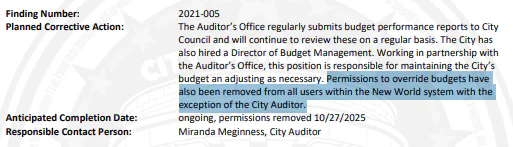

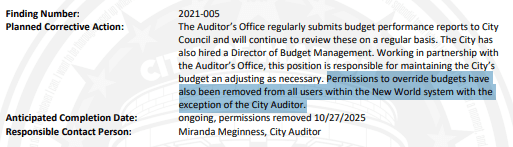

“Permissions to override budgets have also been removed from all users within the New World system with the exception of the City Auditor. Anticipated Completion Date: ongoing, permissions removed 10/27/2025.”

October 27, 2025. That is the date the budget-checking override permissions were finally restricted. Sixteen years, three months, and twenty-six days after New World went live. Every user in the system had override authority for the entire duration.

Every budget ceiling was advisory, not mandatory.

Every appropriation limit was a suggestion.

Veritas Solutions Group was brought in to investigate the ERP configuration, but its work was reportedly hindered. The full scope of what Veritas found—and what prevented them from completing their assessment—is within council summaries, with some remaining a matter for public records requests.

The receipts have been here the entire time. The Auditor of State documented every failure, year after year, finding after finding. What follows is the complete record.

The Complete Record: Every Auditor of State Finding and Reporting Error, 2009–2021

What follows is every formal finding issued by the Ohio Auditor of State for the City of Marion from 2009 through 2021, plus every category of financial reporting error documented in the City’s self-produced reports during the 2017–2019 gap years. For each item, we provide: the finding number and title, a verbatim Auditor quote (or data point from the City’s own report), a plain-language explanation for a general audience, and a forensic IT analysis explaining how New World ERP misconfiguration, disabled controls, or process bypasses would produce the observed result. All ERP module references use verified Tyler Technologies New World module names and architecture.

Audit Year 2009: The New System Arrives — 11 Findings

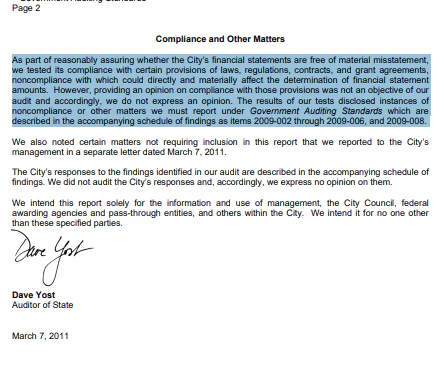

The City of Marion implemented the New World ERP accounting system in July 2009. The Auditor of State’s audit for the year ended December 31, 2009 was filed March 7, 2011. It contained 11 findings — 8 related to generally accepted government auditing standards (GAGAS) and 3 related to federal program compliance under OMB Circular A-133.

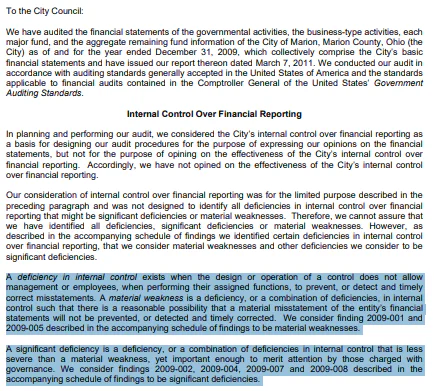

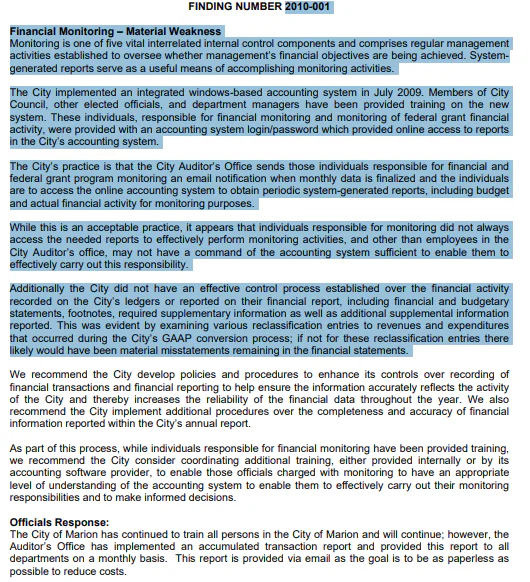

Finding 2009-001: Financial Monitoring — Material Weakness

“The City did not have an effective control process established over the financial activity recorded on the City’s ledgers or reported on their financial report.”

Plain-Language Explanation. The City implemented a brand-new accounting system in July 2009, but the officials responsible for monitoring the City’s finances — Council members, elected officials, department managers — were given only limited training on how to use it. When the Auditor of State examined the City’s financial records, significant reclassification entries were needed to correct revenue and expenditure amounts during the GAAP conversion process. These errors demonstrated that nobody was effectively watching the financial output of the new system.

The City’s response acknowledged the problem: “The City of Marion agrees that additional trainings will be beneficial.” This was the first of many promises to improve that would go unfulfilled for years.

Forensic New World ERP IT Analysis. New World ERP’s General Ledger includes built-in reporting tools and configurable role-based dashboards that provide budget-vs-actual comparison reports, fund balance alerts, and transaction exception flags for elected officials and department managers. These tools were installed as part of the system implementation but were not utilized. The finding indicates that role-based dashboards were not set up, automated exception reports were not scheduled, and variance alerts were not configured. Officials received system login credentials but no structured reporting — the equivalent of handing someone the keys to a car without telling them it has a dashboard.

Per Government Finance Officers Association (GFOA) best practices and the Committee of Sponsoring Organizations (COSO) internal control framework, monitoring activities should be ongoing and embedded in routine operations. In an ERP environment, this requires the system to automatically generate and distribute exception reports — including transactions over a threshold, budget line items approaching their limit, and unusual journal entries. Because these installed features were not configured, monitoring depended entirely on manual processes that Marion had not established.

These articles are fact-based, very well-documented, and have been covering this specific situation since…

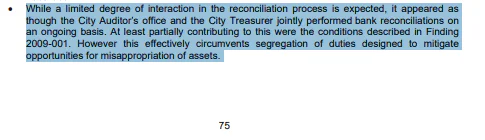

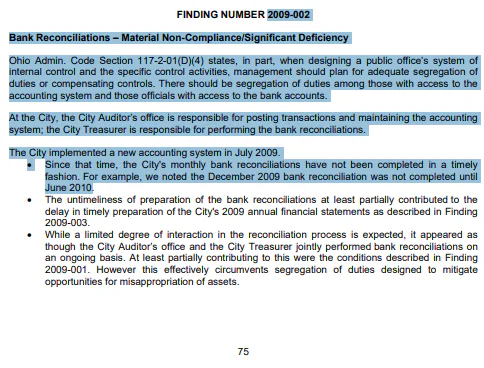

Finding 2009-002: Bank Reconciliations — Material Non-Compliance / Significant Deficiency

“The City implemented a new accounting system in July 2009. Since that time, the City’s monthly bank reconciliations have not been completed in a timely manner.”

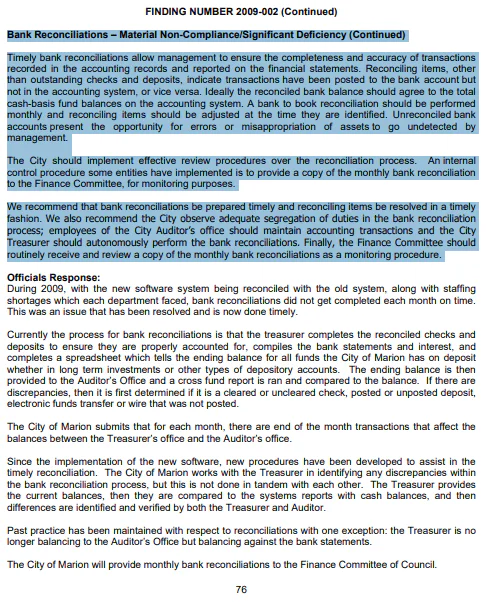

Plain-Language Explanation. Bank reconciliation is the most fundamental financial control in government: comparing what the bank says the City has against what the City’s own books say. After implementing New World, the City stopped performing this reconciliation in a timely manner. Worse, the City Auditor’s office and the City Treasurer were jointly performing reconciliations — combining two offices that are supposed to serve as checks on each other. As the Auditor noted: “Unreconciled bank accounts present the opportunity for errors or misappropriation of assets to go undetected.”

The City’s defense was revealing: “The City of Marion recognizes when working within two systems there could be room for oversight. With the City of Marion now on one system, internal controls are tighter.” They were claiming the problem was the transition — not the new system itself. The next twelve years of audit findings would prove otherwise.

Forensic New World ERP IT Analysis. New World ERP includes a Cash Management module with a Bank Reconciliation program that imports bank statement data (via electronic file or manual entry) and matches transactions against the General Ledger. While this is a distinct component of the suite, it is essential for automated financial oversight. Because the City of Marion did not utilize this module during the initial implementation, bank reconciliation was performed entirely as a manual process outside the system using spreadsheets.

The Bank Reconciliation program requires specific configuration to be functional: bank account mapping to GL accounts, transaction matching rules, outstanding item tracking, and user role assignments that enforce segregation of duties (one role imports bank data, another reviews matches, a third approves). The fact that the Auditor and Treasurer were jointly performing reconciliations confirms that the module was not configured or utilized, forcing a manual workaround that destroyed the segregation of duties the system was designed to enforce. The 2021 corrective action plan confirms that the City eventually began “processing bank reconciliations within the software system, New World” — establishing that this functional module had not been used for the preceding twelve years.

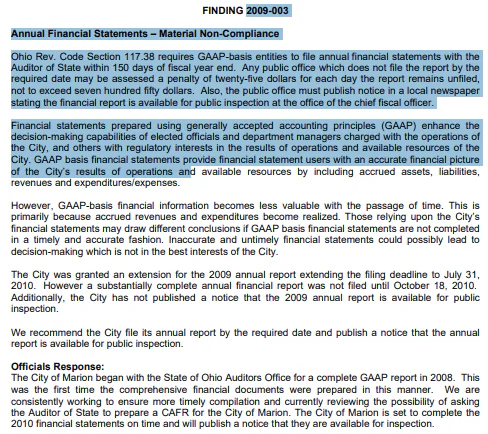

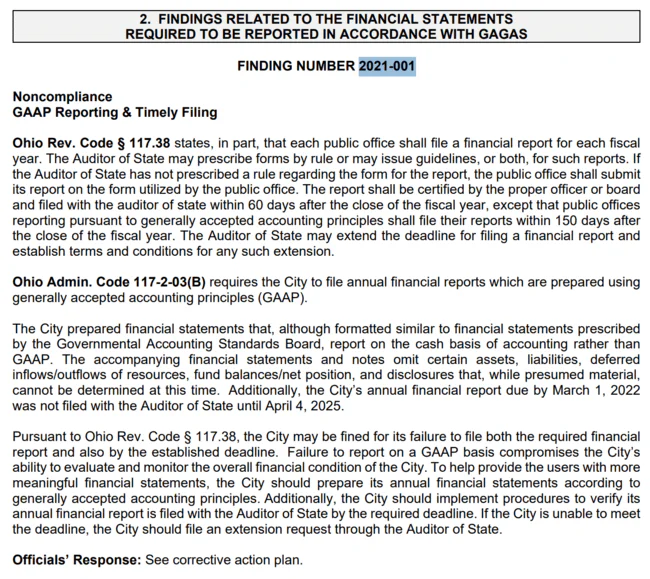

Finding 2009-003: Annual Financial Statements — Material Non-Compliance

“Ohio Rev. Code Section 117.38 requires GAAP-basis entities to file annual financial statements with the Auditor of State within 150 days of fiscal year end.”

Plain-Language Explanation. The City failed to file its annual financial statements on time. Under Ohio law, GAAP-basis financial statements must be submitted to the Auditor of State within 150 days of year-end (approximately May 30 for a December 31 fiscal year). Late filing means financial information becomes stale and less useful for decision-making. The City may also be assessed a $25 per day penalty.

Timely financial reporting is the foundation of government accountability. When a city cannot produce its financial statements on schedule, it signals that either the accounting records are not being maintained in a condition that allows timely reporting, or that the resources and expertise to compile GAAP-basis statements are not available.

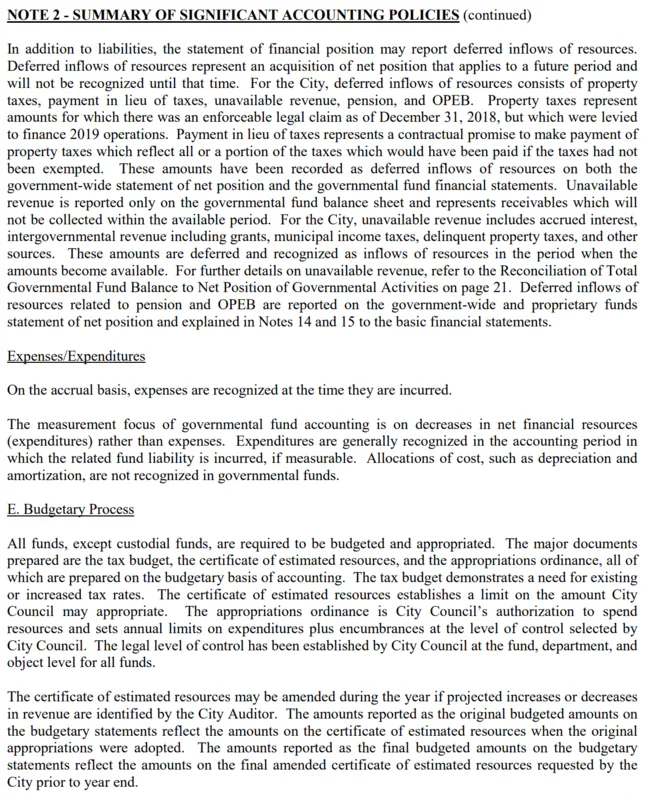

Forensic New World ERP IT Analysis. GAAP-basis financial statements require the ERP to maintain accrual-basis records alongside cash-basis records. In New World, the General Ledger includes a Financial Statement Designer that generates balance sheets, income statements, and statements of cash flows in user-configured formats. However, producing GAAP-basis statements requires that the chart of accounts be structured to track accrual-basis transactions — depreciation schedules, accrued liabilities, deferred revenues, and compensated absences — alongside the cash-basis transactions that drive daily operations.

Because the chart of accounts was configured for cash-basis accounting only during the July 2009 implementation, year-end GAAP financial statement preparation became a labor-intensive manual process requiring extensive adjusting entries outside the system’s normal workflow. This structural limitation explains the late filing — the system was not set up to produce the required output efficiently.

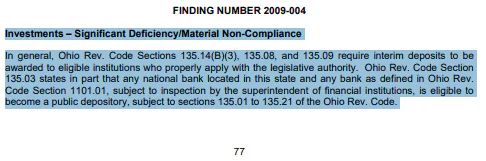

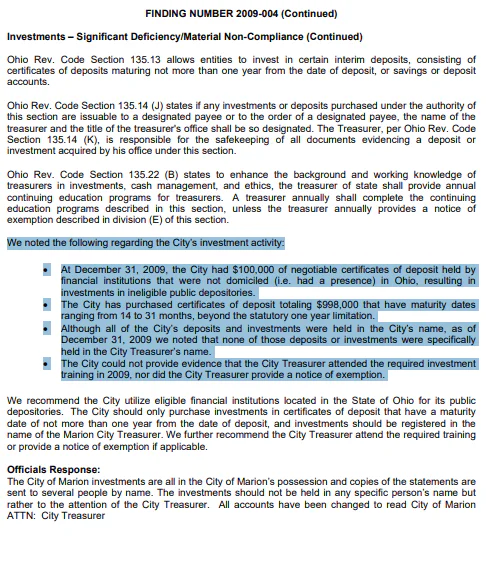

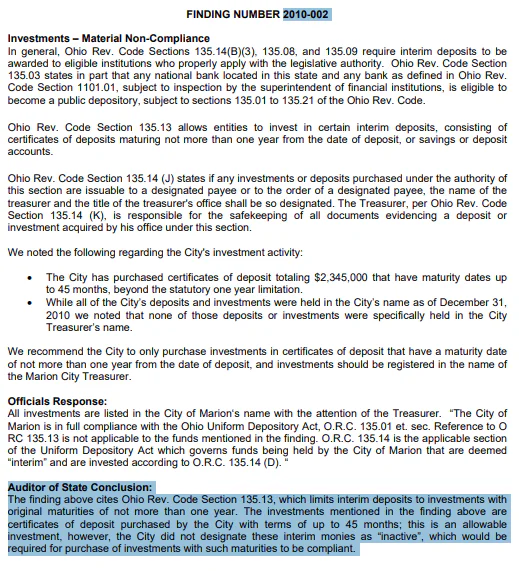

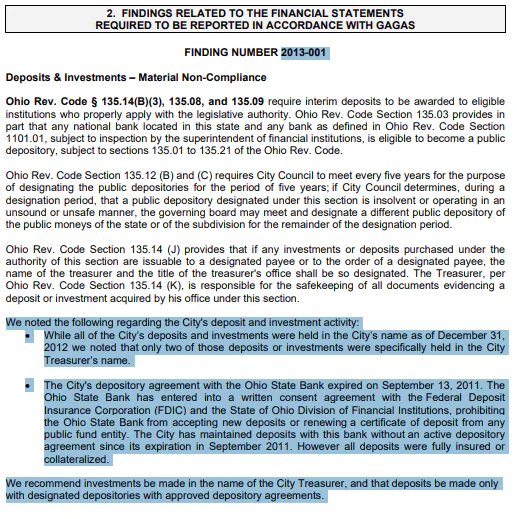

Finding 2009-004: Investments — Significant Deficiency / Material Non-Compliance

“Ohio Rev. Code Sections 135.14(B)(3), 135.08, and 135.09 require interim deposits to be awarded to eligible institutions who properly apply with the legislative authority.”

Plain-Language Explanation. Ohio law requires cities to follow specific procedures for investing public funds — designating approved depositories every five years, awarding deposits through a competitive process, and maintaining proper documentation. The City did not follow these procedures. Certificate of deposit monies were not properly designated, and investment procedures did not comply with the Ohio Revised Code.

Investment compliance is not optional — it protects public funds from being placed in unauthorized or inadequately collateralized institutions. When these procedures are not followed, taxpayer money may be at risk in ways that are not transparent to the public or to Council.

Forensic New World ERP IT Analysis. New World’s Cash Management module includes investment tracking capabilities that monitor investment maturities, track authorized depositories, and generate compliance deadline alerts. Because these investment tracking features were not configured, the ERP did not generate alerts when certificates of deposit matured or when depository authorization periods expired. The City relied on manual tracking for compliance deadlines, which predictably failed.

Per GFOA investment policy best practices, investment tracking should be systematic and automated. The absence of system-driven compliance tracking for a requirement as straightforward as a five-year depository designation cycle indicates that basic compliance calendaring was not established in the ERP during implementation, despite the system having the functional capacity to handle these tasks.

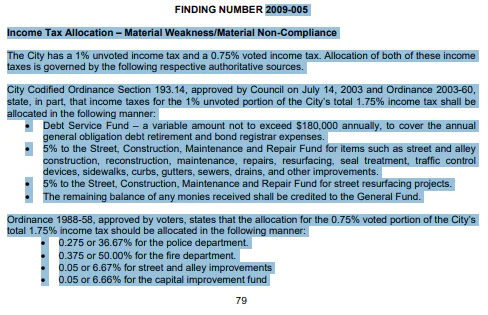

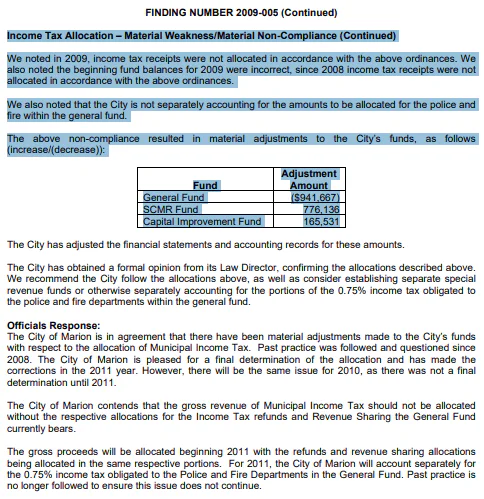

Finding 2009-005: Income Tax Allocation — Material Weakness / Material Non-Compliance

“Income tax receipts were not allocated in accordance with the above ordinances. We also noted the beginning fund balances for 2009 were incorrect, since 2008 income tax receipts were not allocated in accordance with the above ordinances.”

Plain-Language Explanation. The City of Marion has a 1% unvoted income tax and a 0.75% voted income tax, with allocations governed by City Codified Ordinance Section 193.14 and Ordinance 2003-60. These ordinances specify exactly how income tax revenue must be distributed across City funds — specific percentages to the General Fund, police, fire, capital improvements, and debt service. The City was not distributing income tax revenue according to these legally required percentages, and the problem predated the new system — 2008 allocations were also wrong, meaning the opening fund balances in the new system were incorrect from day one.

Income tax is Marion’s largest revenue source. When it is allocated to the wrong funds, every downstream financial decision based on fund balances is potentially wrong — budget appropriations, spending authorizations, transfers, and debt service coverage calculations all depend on accurate fund balances.

Forensic New World ERP IT Analysis. Income tax allocation in New World requires configuring revenue distribution rules in the General Ledger that automatically split incoming tax receipts across the correct funds per ordinance percentages. This is a configuration task performed during implementation: the GL requires a revenue distribution table that maps each income tax receipt type to its required fund allocations based on the percentage split defined in the City’s ordinances.

Because the allocation tables were not configured during the July 2009 migration—and the legacy system’s allocation logic was not replicated in New World—every tax receipt posted to a single fund (the General Fund) rather than being distributed per ordinance. The fact that 2008 allocations were also incorrect confirms the error was carried forward during data migration, compounding the problem. The City was not separately accounting for police and fire allocations within the General Fund, which establishes that the GL’s fund structure was not set up with the required sub-fund or account-level detail to track these allocations.

The intentional misconfiguration of the New World Software and concealment of its flaws ARE THE SILENT SABOTAGE!

Related Silent Sabotage Articles (updated…

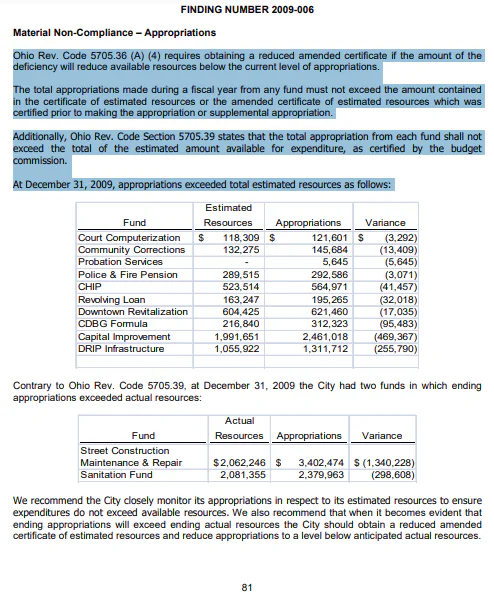

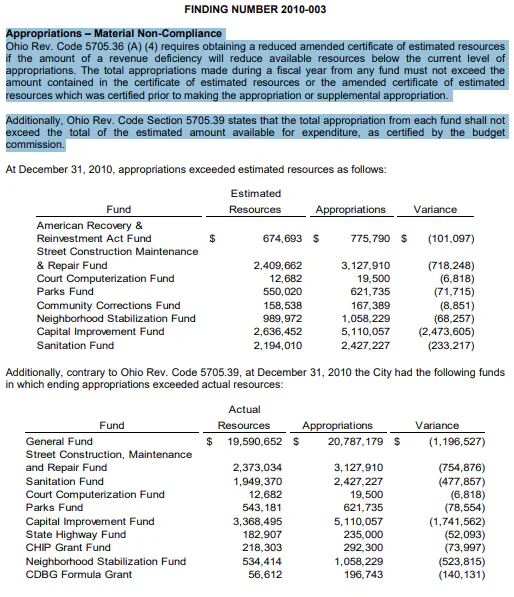

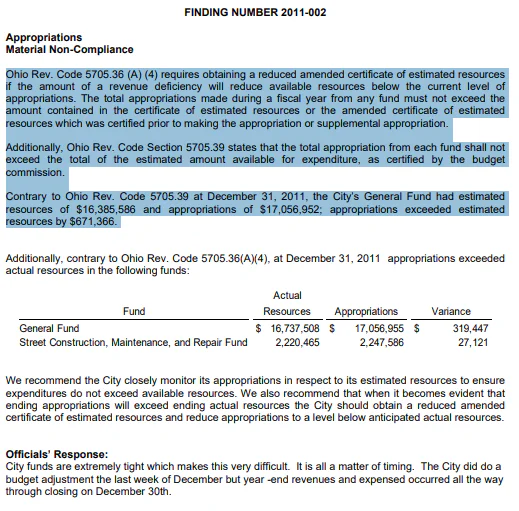

Finding 2009-006: Appropriations — Material Non-Compliance

“At December 31, 2009, appropriations exceeded total estimated resources.”

Plain-Language Explanation. Ohio Revised Code Section 5705.36(A)(4) prohibits a city from appropriating more money than it has available. The County Budget Commission certifies how much revenue a city expects to receive, and appropriations cannot exceed that certified amount. At year-end 2009, Marion’s appropriations were higher than its certified available resources — meaning the City had legally authorized more spending than it had revenue to support.

When appropriations exceed resources, the City is essentially writing checks it knows it may not be able to cash. Ohio law requires the City to obtain a reduced amended certificate from the Budget Commission if revenue falls short, but Marion did not take this step.

Forensic New World ERP IT Analysis. New World’s Budgeting module and the Purchasing module’s budget-checking feature enforce a validation that compares entered appropriations against the certified revenue estimate from the County Budget Commission. This requires configuring the budget-checking validation to reference the certificate of estimated resources as a ceiling. Because this configuration was not active, the system allowed appropriations to be entered at any level without generating a warning or block when they exceeded available resources.

This is a system configuration choice — budget-checking is designed to validate at multiple levels (fund, department, object code) and against multiple thresholds (appropriation, estimated revenue, cash balance). Because the certificate-level validation was not configured, appropriations were entered as free-form amounts with no systemic enforcement of the legal ceiling.

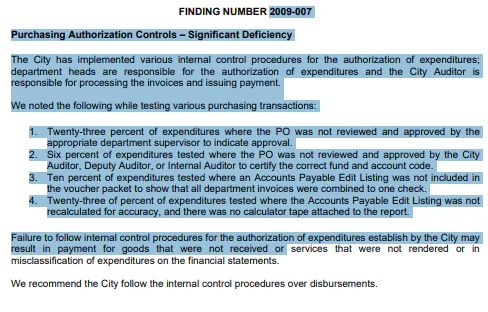

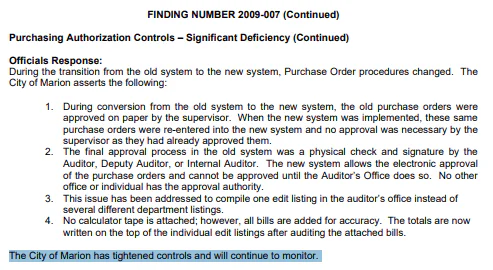

Finding 2009-007: Purchasing Authorization Controls — Significant Deficiency

“Twenty-three percent of expenditures where the PO was not reviewed and approved by the appropriate department supervisor to indicate approval.”

Plain-Language Explanation. Nearly one in four purchase orders was processed without the required supervisor approval. Additionally, 6% of expenditures were not approved by the City Auditor, Deputy Auditor, or Internal Auditor, and 10% of AP Edit Lists were not reviewed. The City’s explanation was telling: “During conversion from the old system to the new system, the old purchase orders were approved on paper by the supervisor. When the new system was implemented, these same purchase orders were re-entered into the new system and no approval was necessary.”

In other words, when purchase orders were migrated from the legacy system to New World, the system did not require them to go through the approval workflow again. This created a massive gap — thousands of dollars in spending authority entered the new system pre-approved, bypassing every digital control the system was supposed to enforce.

Forensic New World ERP IT Analysis. This is a critical ERP configuration failure rooted in the data migration process. New World’s Purchasing module supports configurable multi-level approval workflows. Per Tyler Technologies documentation, the module “allows configuration of approval workflows on various aspects of the requisition, including department, GL account, commodity code and project account.” Users are designated with or without “supervisor rights” — those without supervisor rights must have their transactions approved before the City Auditor’s office processes them.

During migration, the purchase orders re-entered from the legacy system were required to be routed through the standard approval workflow regardless of their prior approval status. Because they were entered as pre-approved, the migration process was configured to bypass the approval chain — likely to expedite the transition. This “temporary” bypass created a permanent control gap: 23% of POs had no supervisor approval. Additionally, the ongoing 6% bypass rate for City Auditor approval establishes that the approval workflow rules were not configured as mandatory — the system allowed transactions to proceed without all required approvals.

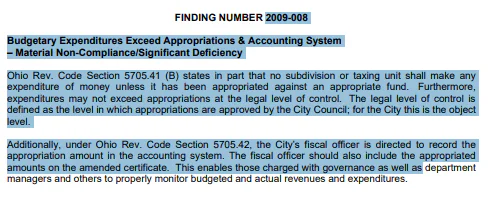

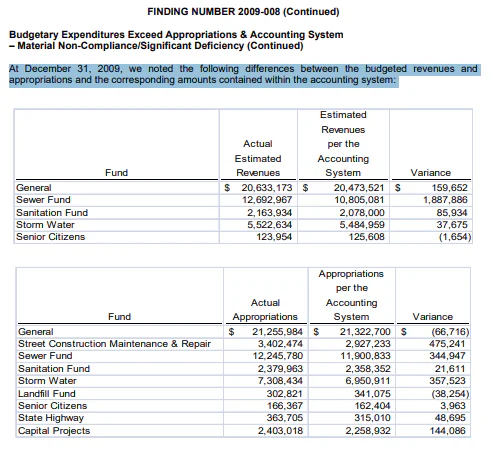

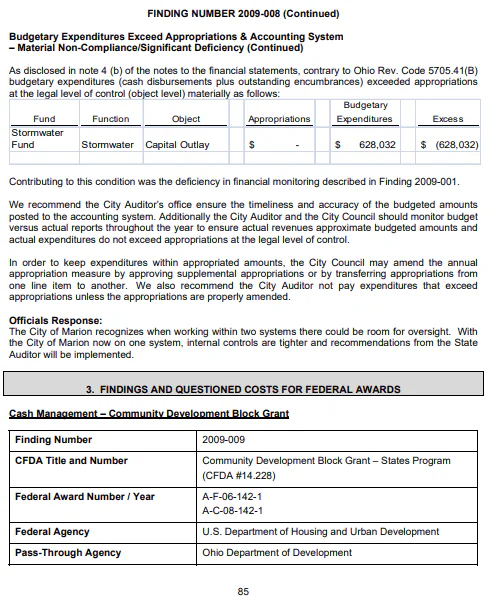

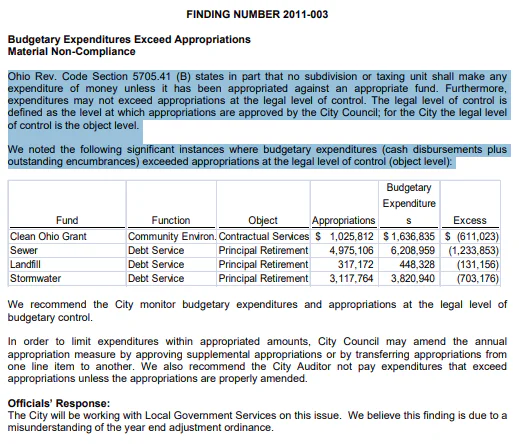

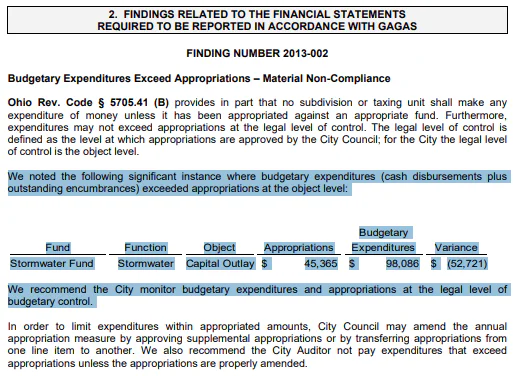

Finding 2009-008: Budgetary Expenditures Exceed Appropriations & Accounting System — Material Non-Compliance / Significant Deficiency

“Budgetary expenditures (cash disbursements plus outstanding encumbrances) exceeded appropriations at the legal level of control (object level) materially.”

Plain-Language Explanation. This is the finding that would define Marion’s financial collapse for the next sixteen years. Expenditures exceeded the amounts legally appropriated by Council — not by small amounts, but “materially,” meaning the overages were large enough to matter. Ohio law prohibits spending more than what has been appropriated at the legal level of control (the object code level within each fund). The City also had unexplained differences between budgeted revenues and appropriations in the accounting system versus the amounts on file with the County Budget Commission.

The City’s response: “The City of Marion recognizes when working within two systems there could be room for oversight.” They blamed the dual-system transition. But the budget override capability is a feature of the new system — it was New World that allowed the overspending, not the legacy system.

Forensic New World ERP IT Analysis. This is the first documented instance of the budget override problem that persisted until October 27, 2025. New World’s Purchasing module performs budget-checking during purchase order and requisition entry. Per Tyler Technologies documentation, the system “provides budget-checking at the individual account or group budget segment level during requisition input with override capabilities.” The override is a designed feature — not a bug — that exists to allow authorized personnel to process legitimate emergency expenditures when budget-checking indicates insufficient appropriation.

The control failure in Marion was not that the override existed — it was that override permissions were assigned too broadly. Every user with spending authority had the ability to override budget-checking. Per industry best practice (GFOA, GAQC, and state auditor guidance), override authority is restricted to one or two senior officials (typically the Finance Director or City Auditor), with all override events logged and reviewed by an independent party. In Marion, the override was unrestricted, and the override log was not reviewed. This single configuration decision — leaving override permissions open to all users — is the root cause of the finding that repeated until 2025.

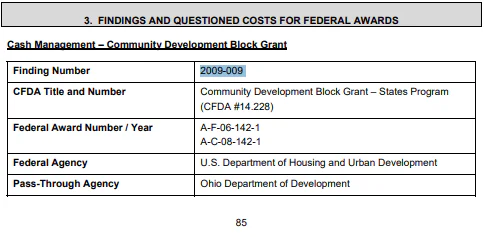

Finding 2009-009: Federal — Financial Monitoring — Material Weakness

“See finding 2009-001; A-133 requires separate reporting of this material weakness for federal programs.”

Plain-Language Explanation. OMB Circular A-133 (the federal Single Audit standard) requires that material weaknesses in internal controls be separately reported for federal programs. The financial monitoring failure documented in Finding 2009-001 affected not just City funds but every federal grant the City administered. This finding ensures the federal dimension of the monitoring failure is formally on the record.

For federal grantor agencies, a material weakness in financial monitoring means the City cannot demonstrate adequate stewardship of federal funds. This can affect future grant eligibility, require additional monitoring by the grantor, or trigger grant-specific audit requirements.

Forensic New World ERP IT Analysis. The same General Ledger reporting and dashboard configuration gaps that caused Finding 2009-001 have amplified consequences for federal programs. Federal grants require dedicated monitoring — real-time expenditure tracking against grant budgets, compliance with specific cost principles, and periodic reporting to grantor agencies. New World’s Project Accounting module provides grant-specific budget monitoring, but this requires each grant to be set up as a separate project with its own budget, revenue, and expenditure tracking. Because this configuration was not utilized, federal grant monitoring depended on the same inadequate general monitoring that was already failing for City funds.

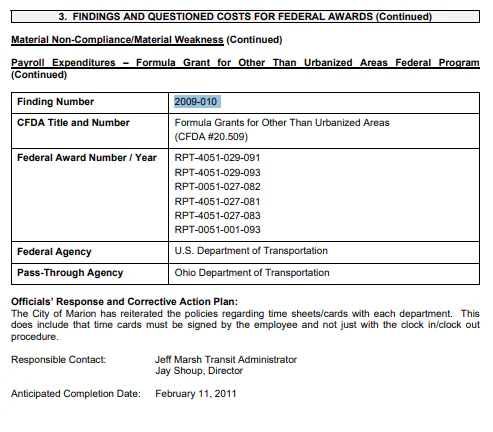

`Finding 2009‑010 — Payroll Expenditures, Formula Grant (Material Weakness / Material Non‑Compliance)

“Transit Department Payroll did not follow established procedures and was not documented in accordance with federal requirements.”

Plain‑language Explaination:

This finding means the city was charging payroll costs to a federal transit grant without following the rules that come with that money. Staff in the Transit Department were not documenting time, pay, or cost allocations in the way federal regulations require. That could include missing timesheets, incomplete support for which employees were working on which grant‑funded activities, or lump‑sum charges with no backup.

When payroll is not documented correctly, federal reviewers cannot tell whether the grant is paying only for eligible work. That opens the door to “disallowed costs”—money the city might have to pay back. It also signals that internal oversight over one of the largest recurring expenses (payroll) was weak, especially where federal funds were involved.

Forensic New World ERP IT Analysis:

In a properly configured ERP, the HR/payroll module is tightly integrated with grant accounting. Employees working on grant‑funded programs are assigned to specific cost centers or project codes, and their time entries flow automatically into the grant ledger with required documentation. Because New World was not configured with those cost centers, or because staff were allowed to bypass them and post lump‑sum journal entries instead, the system did not enforce federal documentation standards.

This finding establishes that the grant‑specific payroll configuration was not completed in New World, and users were allowed to override it with manual postings. Missing workflow requirements—such as mandatory timesheet approvals, required grant codes on payroll batches, and automated exception reports—allowed undocumented payroll charges to hit the grant. In other words, the ERP was not used as a compliance engine for federal payroll; it was treated as a generic check‑writer, with the federal rules effectively turned off.

Finding 2009-011: Federal — Material Weakness in Internal Control Over Compliance

“We consider the deficiencies described as items 2009-009 through 2009-011 to be material weaknesses in internal control over compliance.”

Plain-Language Explanation. This is an aggregate finding classifying multiple federal internal control deficiencies as material weaknesses. The Auditor concluded that the City’s internal controls over federal program compliance were so deficient that there was a reasonable possibility material noncompliance could occur and not be detected. This is the most severe classification available — it signals to federal grantor agencies that the City cannot be trusted to manage federal funds without significant remediation.

Forensic New World ERP IT Analysis. Federal programs require specific internal controls including segregation of duties, expenditure authorization, matching/earmarking compliance, and financial monitoring. New World’s security permission system enforces role-based access that separates incompatible duties. For federal fund accounting, the Project Accounting and Grant Management modules include grant-specific approval workflows, expenditure limits, and compliance tracking.

The aggregate nature of this material weakness finding demonstrates that none of these federal-specific configurations were implemented. The ERP was deployed without utilizing the functional capabilities necessary for the City’s federal compliance obligations.

Finding 2009-012: Federal — Purchasing Authorization Controls — Significant Deficiency

“We consider the deficiency described as item 2009-012 to be a significant deficiency in internal control over compliance.”

Plain-Language Explanation. The same purchasing authorization control failure documented in Finding 2009-007 (23% of POs without supervisor approval) is reported separately for federal compliance purposes. Federal grants require documented approval chains per OMB cost principles — every expenditure charged to a federal grant must have documented authorization. When 23% of POs lack supervisor approval, every one of those POs that was charged to a federal grant represents a potential questioned cost.

Forensic New World ERP IT Analysis. The Purchasing module’s configurable approval workflow includes grant-specific approval rules for federal programs. When a purchase order references a federal grant fund or project code, the workflow routes through additional approval levels — including the grant administrator and the fiscal officer responsible for federal compliance. The same migration-era bypass that allowed 23% of POs through without supervisor approval also bypassed these grant-specific approval requirements, making every federal expenditure during the migration period a compliance risk.

Audit Year 2010: The Problems Multiply — 22 Findings

The Auditor of State’s audit for the year ended December 31, 2010 was filed October 20, 2011. It contained 22 findings — 10 related to GAGAS and 12 related to federal program compliance. The finding count more than doubled from the first year, and new categories of failure emerged: negative fund balances, cross-fund payments, and an expanding range of federal compliance breakdowns.

Finding 2010-001: Financial Monitoring — Material Weakness (Repeat)

“The City implemented an integrated windows-based accounting system in July 2009. Members of City Council, other elected officials, and department managers have been provided training on the new system.”

Plain-Language Explanation. Second consecutive year of this finding. The City had given officials login credentials and online access to system-generated reports, but monitoring remained inadequate. Having access to a system is not the same as having a system configured to surface the right information at the right time to the right people.

Forensic New World ERP IT Analysis. Providing login credentials without configuring the General Ledger’s reporting tools and role-based dashboards is like giving someone a library card without a catalog. New World pushes automated exception reports — budget overrun alerts, unusual transaction flags, and fund balance warnings — to user dashboards. The fact that officials had access but monitoring remained deficient establishes that the alert and reporting configuration was never completed. The system generated data, but it did not generate insight because the configuration required to do so was not utilized.

Finding 2010-002: Investments — Material Non-Compliance

“Per Ohio Rev. Code requirements for interim deposits and public depositories.”

Plain-Language Explanation. Second year of investment procedure failures. City Council still had not properly designated public depositories as required by Ohio law. The same compliance gap persisted without correction.

Forensic New World ERP IT Analysis. This is a repeat of Finding 2009-004. The Cash Management module’s investment tracking features remained unconfigured. No compliance deadline tracking was established in the system for the five-year depository designation requirement, despite the system’s functional capacity to automate these alerts.

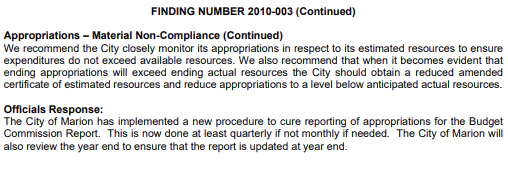

Finding 2010-003: Appropriations — Material Non-Compliance

“At December 31, 2010, appropriations exceeded total estimated resources.”

Plain-Language Explanation. Second consecutive year where the City appropriated more than its certified available resources. The City responded: “The City of Marion has implemented a new procedure to cure reporting of appropriations for the Budget Commission Report.” The use of the word “procedure” — rather than “system configuration” — suggests a manual workaround rather than fixing the underlying budget-checking validation.

Forensic New World ERP IT Analysis. This is a repeat of Finding 2009-006. The Budgeting module’s validation against the County Budget Commission’s certificate of estimated resources remained unconfigured. The City’s claim of a “new procedure” confirms they implemented a manual solution rather than configuring the system to enforce the legal ceiling automatically — a pattern that repeated across many finding categories despite the system’s built-in capability to prevent these overages.

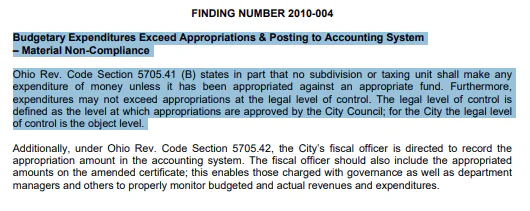

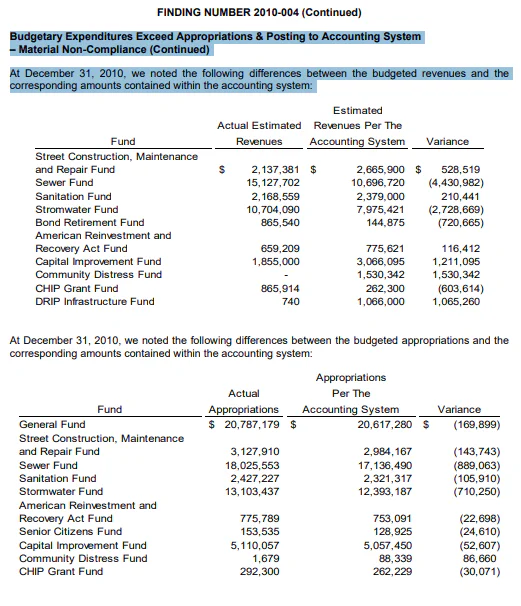

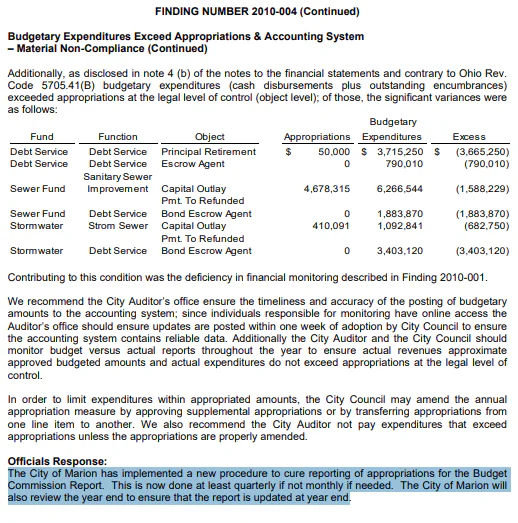

Finding 2010-004: Budgetary Expenditures Exceed Appropriations — Material Non-Compliance

“Expenditures may not exceed appropriations at the legal level of control.”

Plain-Language Explanation. Second year of expenditures exceeding appropriations. The budget override permissions remained active and unrestricted. The same configuration flaw that allowed overspending in 2009 continued without correction.

Forensic New World ERP IT Analysis. The Purchasing module’s budget-checking override permissions remained assigned to all users with spending authority. No action was taken after the 2009 finding to restrict override access. The override audit trail — which New World maintains for every budget-checking override event — was not reviewed by any independent party. This is the same permission setting that remained unrestricted until October 27, 2025.

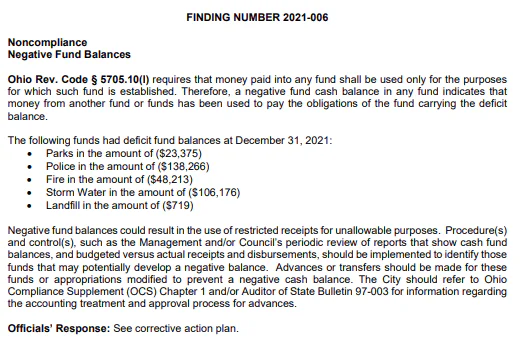

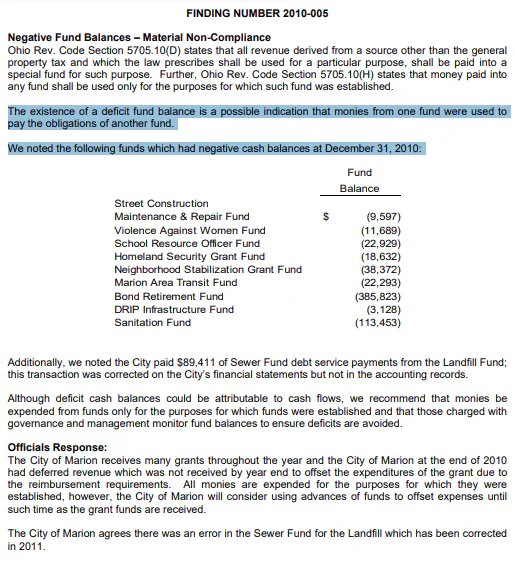

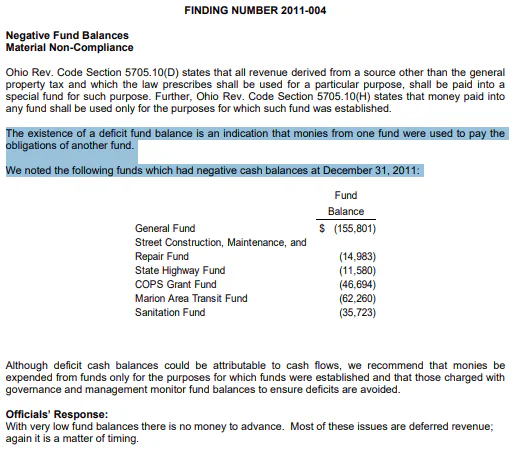

Finding 2010-005: Negative Fund Balances — Material Non-Compliance

“The existence of a deficit fund balance is a possible indication that monies from one fund were used to pay the obligations of another fund.”

Plain-Language Explanation. Multiple funds ended 2010 with negative cash balances. The Auditor specifically identified that the City paid $89,411 of Sewer Fund debt service from the Landfill Fund — a cross-fund payment that used one fund’s money to pay another fund’s obligations. Ohio Rev. Code Section 5705.10(I) requires that money paid into any fund be used only for the purposes for which that fund was established.

Cross-fund payments are not merely bookkeeping errors — they represent unauthorized transfers of public money from one legally restricted purpose to another. Sewer fund revenue comes from sewer ratepayers; landfill fund revenue comes from landfill fees. Using landfill money to pay sewer debt means landfill ratepayers are subsidizing sewer operations without legal authorization.

Forensic New World ERP IT Analysis. New World’s General Ledger fund accounting enforces fund integrity through interfund transfer controls. The system is designed to require Council authorization for any interfund transfer and blocks expenditure transactions that would drive a fund balance below zero. Because the negative-balance control was not configured, the system allowed expenditures to be charged against any fund regardless of available balance. The $89,411 cross-fund payment from Landfill to Sewer was not blocked by the system or flagged as requiring Council authorization because neither control was active.

Per GFOA fund balance policy best practices, the General Ledger generates alerts when any fund balance approaches zero and provides a hard-stop on transactions that would create a deficit. This requires configuring budget-checking validation at the fund level in addition to the account level. The absence of this control enabled systematic cross-fund subsidization.

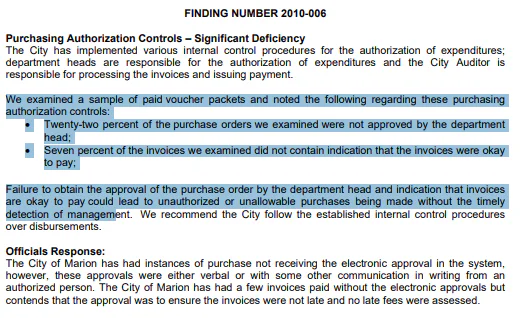

Finding 2010-006: Purchasing Authorization Controls — Significant Deficiency

“Twenty-two percent of the purchase orders we examined were not approved by the department head.”

Plain-Language Explanation. Second consecutive year with approximately one in four purchase orders lacking supervisor approval. Additionally, 7% of invoices did not have an “okay to pay” indication. The Purchasing module’s approval workflow remained unconfigured or unenforced.

Forensic New World ERP IT Analysis. Repeat of 2009-007. The Purchasing module’s configurable approval workflow — which per Tyler documentation supports approval routing based on department, GL account, commodity code, and project account — still was not configured as mandatory. The marginal improvement from 23% to 22% bypass rate suggests no systemic correction was made; the slight change was likely random variation.

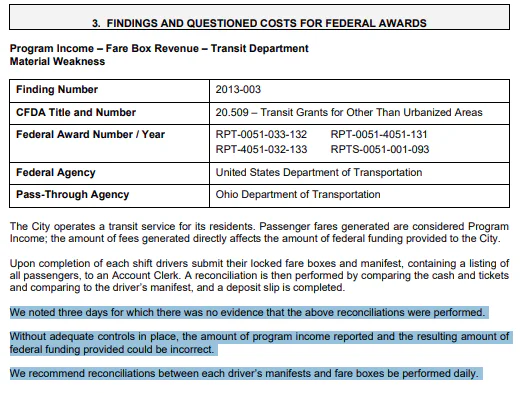

Finding 2010-007: Fare Box Revenue — Transit Department — Significant Deficiency

“See Federal Finding 2010-013 in Section 3 below.”

Plain-Language Explanation. Transit fare box revenue controls were deficient. This GAGAS finding cross-references the detailed federal finding (2010-013) in Section 3 of the audit.

Forensic New World ERP IT Analysis. Revenue receipt controls for the transit department were not configured in the Cash Receipting module. Cash from fare boxes is reconciled against driver manifests with documented counts, variance explanations, and supervisory approval — a process that is tracked in New World’s Cash Receipting module when configured for the transit operation’s specific workflow. Because this specific configuration was not implemented, the system did not provide the necessary oversight for transit revenue, leading to the identified control gaps.

Finding 2010-008: Expenditure Authorization Controls — Transit Department — Significant Deficiency

[Editor’s Note — Finding 2010-015: This finding number is present in the AOS sequential numbering but was omitted from the original article text. Its inclusion raises the FY2010 count from 21 to 22 and the overall formal findings total from 60 to 61. The GAGAS-vs.-federal classification has been inferred as federal based on its sequence position. Verify against the original AOS report.]

“See Federal Finding 2010-016 in Section 3 below.”

Plain-Language Explanation. Transit department expenditure authorization controls were deficient. This cross-references the detailed federal finding addressing time distribution and cost allocation for employees working on multiple federal and non-federal activities.

Forensic New World ERP IT Analysis. Federal grant expenditure controls require time-and-effort documentation per OMB Circular A-87 (now 2 C.F.R. Part 225). New World’s Payroll/HR module includes the ability to require activity codes and time distribution for employees charged to federal grants, but this feature was not set up for federally-funded transit employees. Because these activity code requirements were not active, payroll costs were allocated to grants based on estimates rather than actual time worked, bypassing the system’s functional capacity to enforce federal documentation standards.

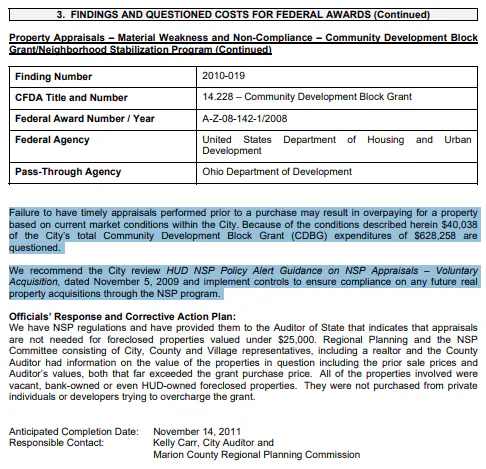

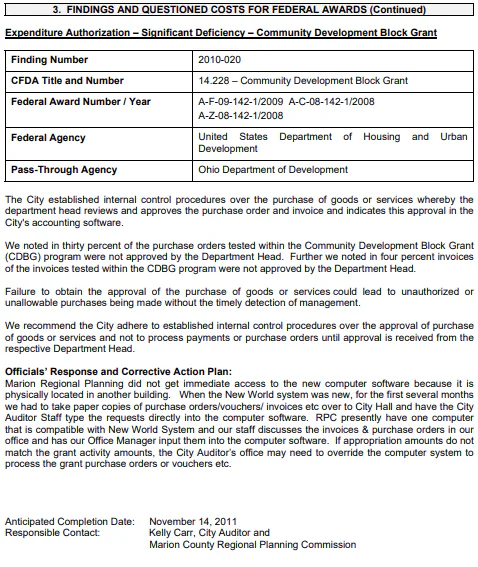

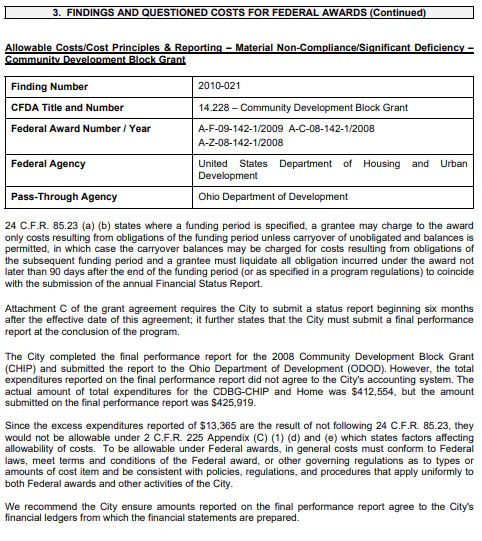

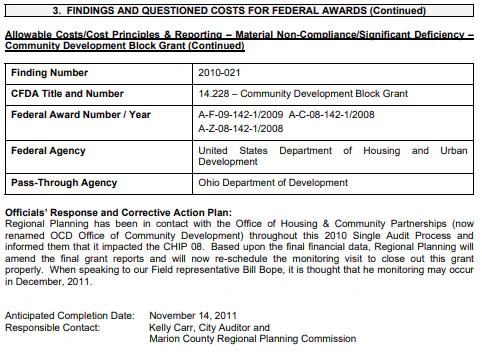

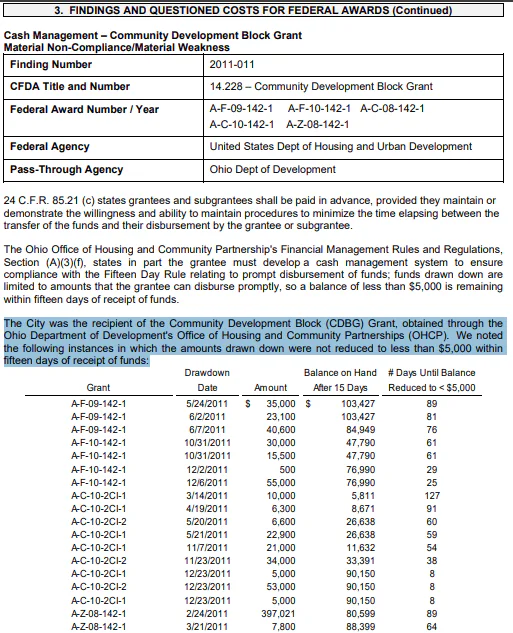

Finding 2010-009: Expenditure Authorization Controls — CDBG — Significant Deficiency

“See Federal Finding 2010-020 in Section 3 below.”

Plain-Language Explanation. Community Development Block Grant expenditure authorization controls were deficient. CDBG expenditures exceeded the grant budget by $13,365.

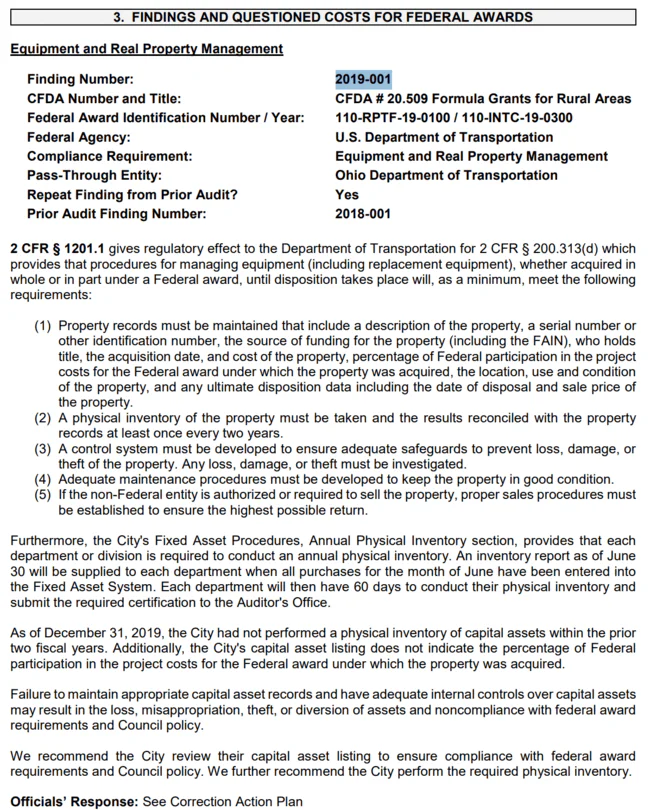

Forensic New World ERP IT Analysis. The same budget-checking override that allows City fund expenditures to exceed appropriations also allows federal grant expenditures to exceed grant budgets. The Project Accounting module—configured for each CDBG grant with grant-specific budget ceilings—enforces spending limits. Because this configuration was not utilized, grant budgets remained unprotected, allowing expenditures to proceed beyond authorized federal limits.

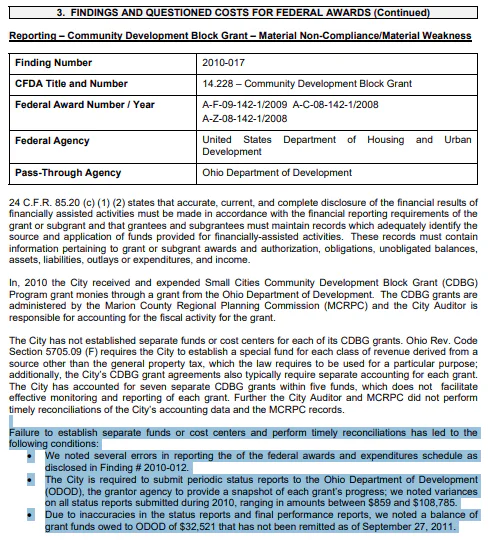

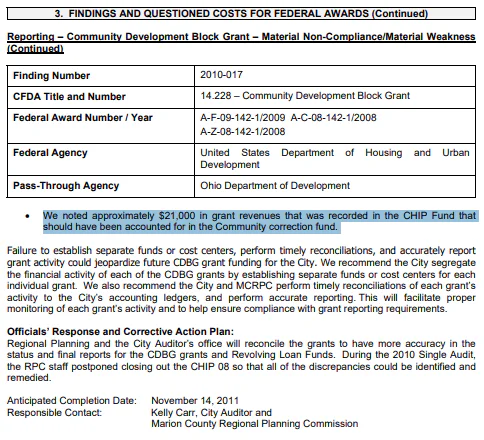

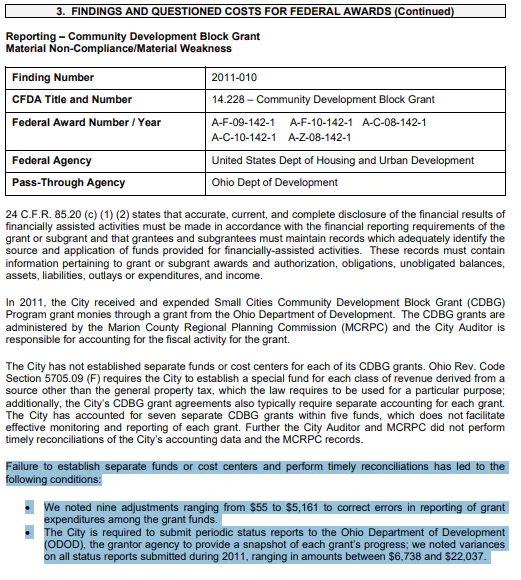

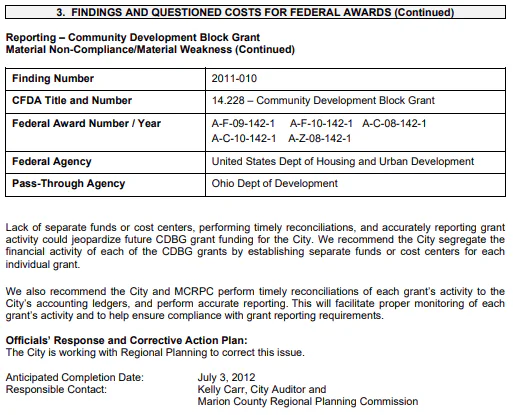

Finding 2010-010: Reporting — CDBG — Material Weakness

“See Federal Finding 2010-017 in Section 3 below.”

Plain-Language Explanation. CDBG reporting was materially deficient. The City could not produce accurate reports of CDBG expenditures by category because grant expenditures were not tracked with sufficient detail in the accounting system.

Forensic New World ERP IT Analysis. Federal grant reporting requires the General Ledger to track expenditures by grant, by budget category, and by reporting period. Because the grant-specific fund codes, cost centers, and project codes were not configured in New World, accurate federal reports could not be generated from the system. The City compiled federal reports manually from incomplete system data — a process that inevitably produced errors.

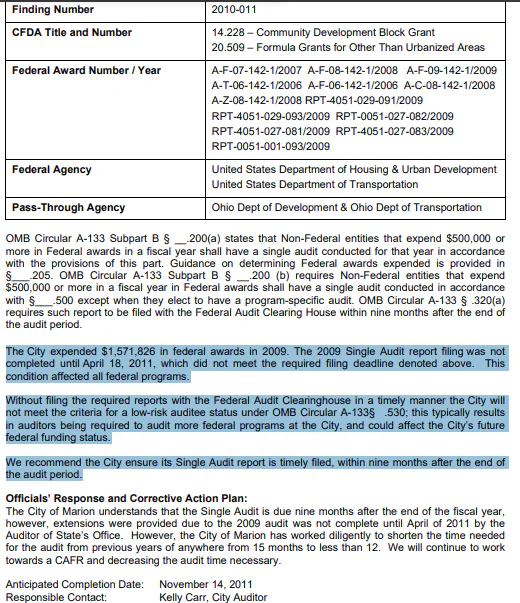

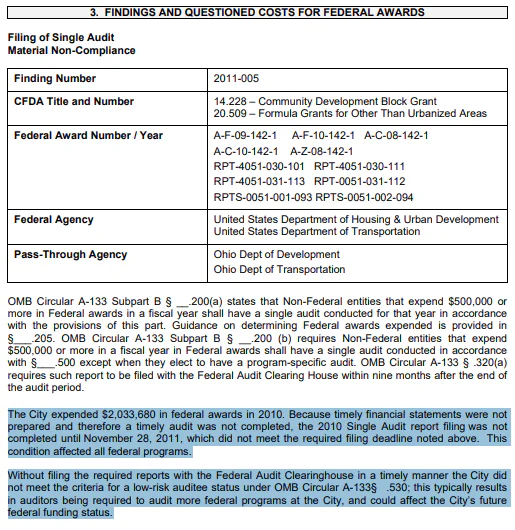

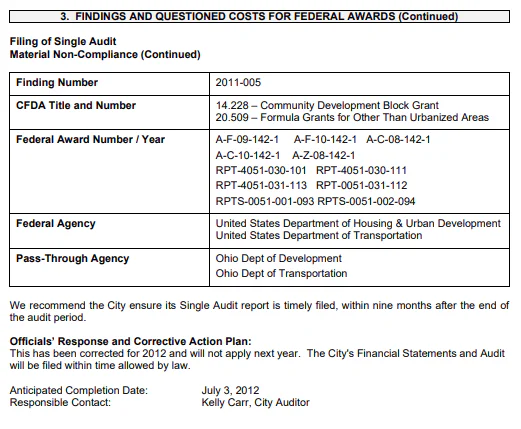

Finding 2010-011: Filing of Single Audit — Material Non-Compliance / Significant Deficiency (Federal)

“The City expended $1,571,826 in federal awards in 2009. The 2009 Single Audit report filing was not completed until April 18, 2011, which did not meet the required filing deadline.”

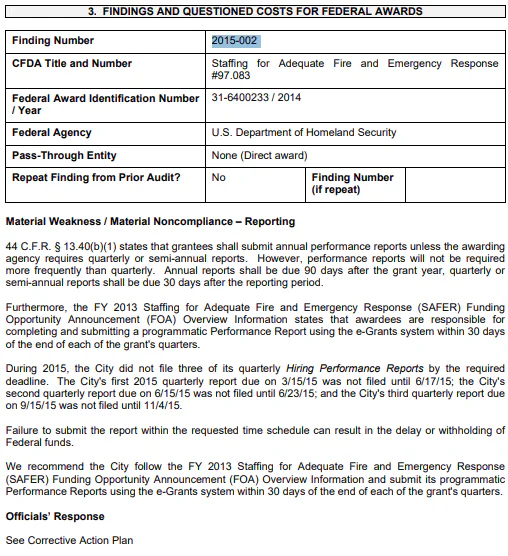

Plain-Language Explanation. OMB Circular A-133 requires the Single Audit to be filed within nine months of fiscal year-end — by September 30, 2010 for fiscal year 2009. The City did not file until April 18, 2011, more than six months late. Late filing affects the City’s status as a “low-risk auditee” and could affect future federal funding eligibility.

Forensic New World ERP IT Analysis. The inability to produce timely financial statements — driven by the ERP configuration issues documented in Findings 2009-001 through 2009-008 — cascaded into late Single Audit filings. When the General Ledger cannot generate clean, reconciled financial data for year-end close, the entire audit process is delayed. The ERP’s year-end close procedures and GAAP reporting capabilities were insufficiently configured to support timely statement preparation.

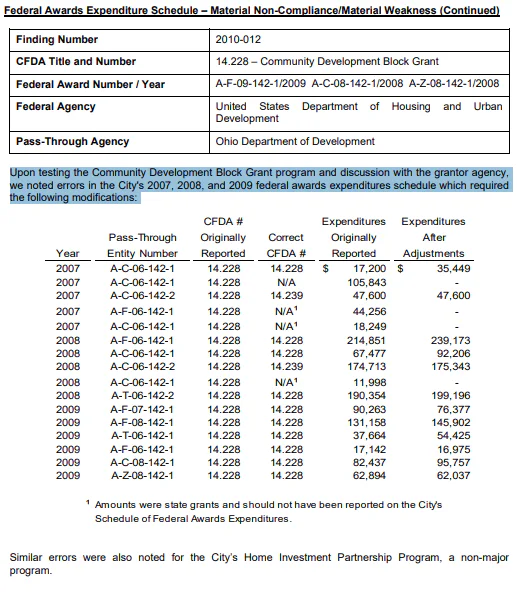

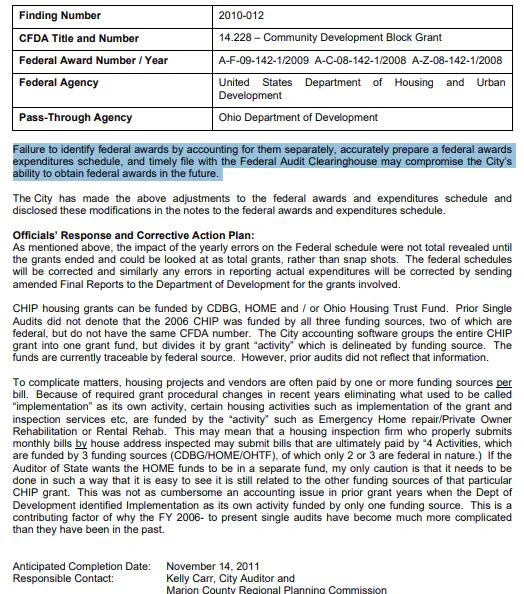

Finding 2010-012: Federal Awards Expenditure Schedule — Material Non-Compliance / Material Weakness (Federal)

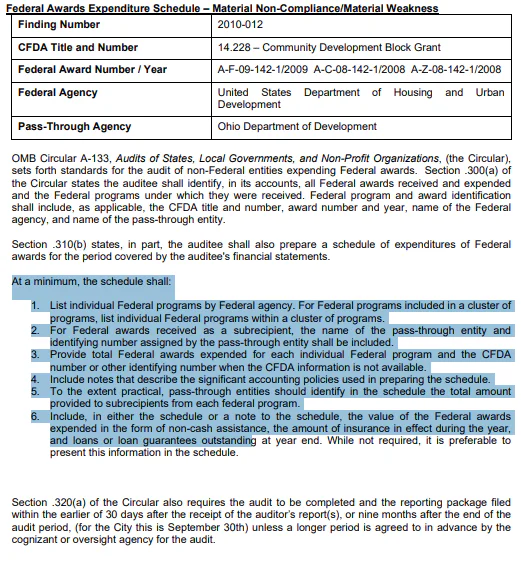

“We noted errors in the City’s 2007, 2008, and 2009 federal awards expenditures schedule.”

Plain-Language Explanation. The Schedule of Expenditures of Federal Awards (SEFA) — required for every Single Audit — contained errors spanning three years. State grants were incorrectly classified on the federal schedule. CDBG, HOME, and Ohio Housing Trust Fund grants were commingled because the City’s accounting system grouped the entire CHIP housing grant into a single fund without distinguishing between federal and state components.

Forensic New World ERP IT Analysis. The General Ledger was not configured with separate fund codes or project codes for each federal grant. When multiple grants are commingled in a single fund, the system cannot generate an accurate SEFA. This is a chart of accounts design failure from implementation — the fund structure did not include sufficient detail to track individual grants. The error spanning 2007–2009 establishes that the configuration was inherited from the legacy system migration without correction, compounding three years of misclassification.

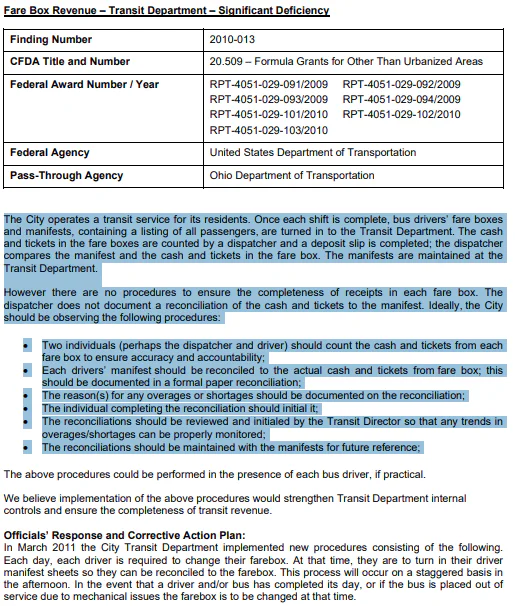

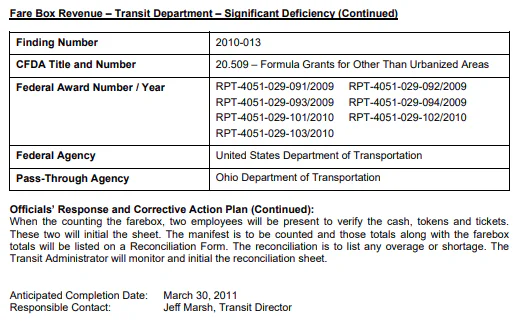

Finding 2010-013: Fare Box Revenue — Transit — Significant Deficiency (Federal)

“There are no procedures to ensure the completeness of receipts in each fare box. The dispatcher does not document a reconciliation of the cash and tickets to the manifest.”

Plain-Language Explanation. No two-person count of fare boxes was being performed. No formal reconciliation existed between driver manifests and fare box contents. Overages and shortages were not documented. The Transit Director did not review fare box reconciliations. This meant there was no way to verify that all cash collected from passengers actually made it into the City’s bank account.

Forensic New World ERP IT Analysis. New World’s Cash Receipting module requires dual-entry for cash deposits: one entry for the manifest count and a second independent entry for the physical cash count. The system flags variances between these two entries for supervisory review. For transit operations, this involves configuring a receipt type that requires both a manifest reference and a cash count, with automated variance calculation and supervisor approval workflow. None of this was configured for the transit department, despite the system’s functional capacity to automate these internal controls.

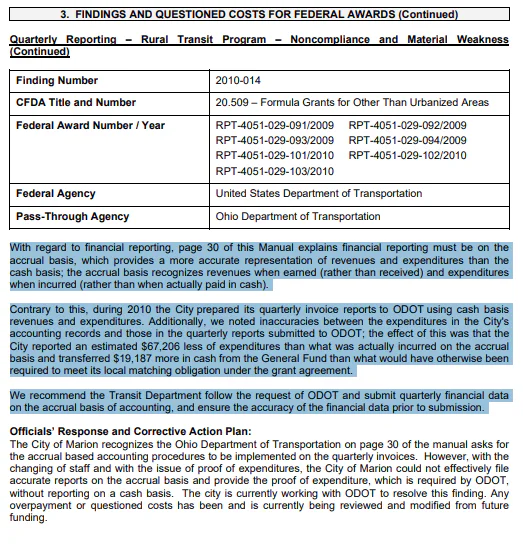

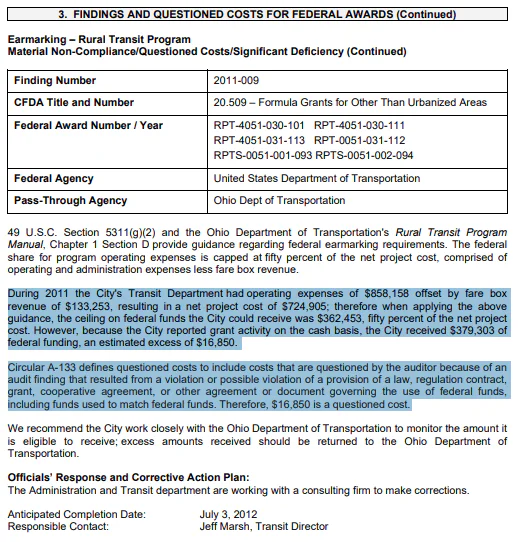

Finding 2010-014: Quarterly Reporting — Rural Transit Program — Noncompliance / Material Weakness (Federal)

“During 2010 the City prepared its quarterly invoice reports to ODOT using cash basis revenues and expenditures” contrary to required accrual basis.

Plain-Language Explanation. The City submitted cash-basis financial data to ODOT for the Rural Transit Program when accrual-basis reporting was required. This understated expenditures by an estimated $67,206 and caused the City to transfer $19,187 more from the General Fund than actually required for the local match. The City blamed “changing of staff” and “issue of proof of expenditures.”

Forensic New World ERP IT Analysis. New World’s General Ledger supports both cash and accrual basis accounting through its chart of accounts configuration. For federal programs requiring accrual-basis reports, the GL is configured to track accruals — accounts payable, accounts receivable, and prepaid expenses — at the grant level. Because the federal grant funds were set up as cash-basis funds (matching the City’s primary accounting method), the system was unable to generate accrual-basis reports without manual adjustment. The Grant Management module maintains the reporting basis requirement for each grant to ensure correct report generation, but this functional capacity was not utilized during the system setup.

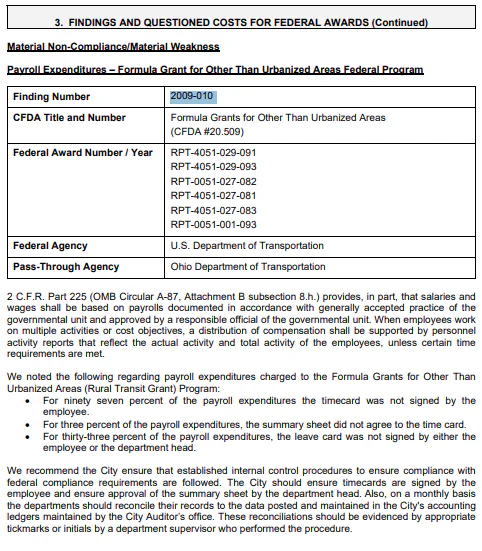

Finding 2010-015 — Payroll Expenditures, Capital Grant (Material Weakness / Material Non-Compliance)

“The Transit Department failed to properly document payroll expenditures charged to the federal capital grant, resulting in non-compliance with federal regulations.”

Plain-Language Explanation.

This finding indicates that payroll costs charged to the federal capital grant were not supported by adequate documentation. Employees’ time and effort were not properly tracked or allocated to grant-funded activities, leading to potential disallowed costs and increased risk of federal funds being improperly used.

Proper documentation is essential to ensure that only eligible payroll costs are charged to the grant. Without it, federal reviewers cannot verify compliance, which may result in financial penalties or repayment obligations.

Forensic New World ERP IT Analysis:

The ERP system enforces grant-specific payroll configurations, including mandatory timesheet approvals and accurate cost center assignments. Because these controls were not configured or enforced, the system allowed manual overrides and lump-sum postings that bypassed federal compliance requirements.

This finding establishes gaps in the ERP’s payroll module configuration for the capital grant and an absence of required system processes, undermining the system’s role as a compliance tool for federal payroll expenditures.

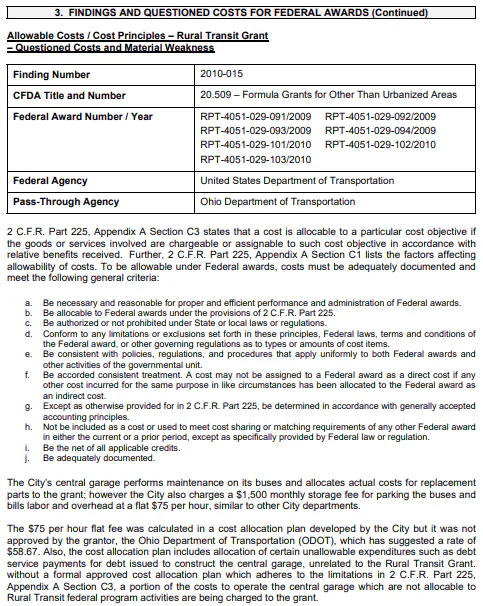

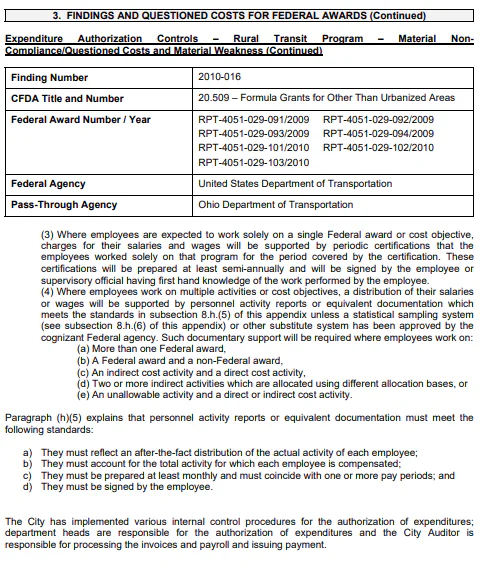

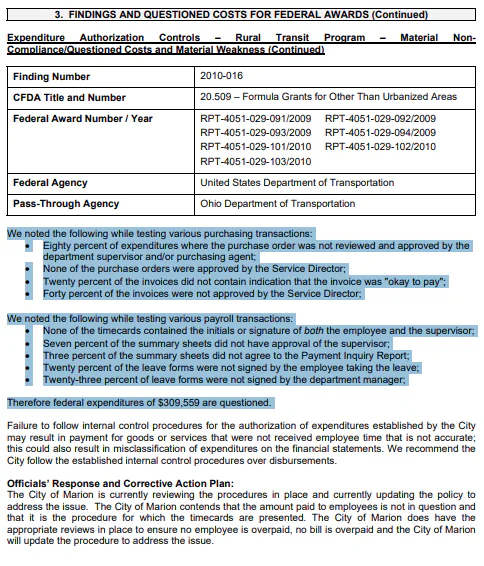

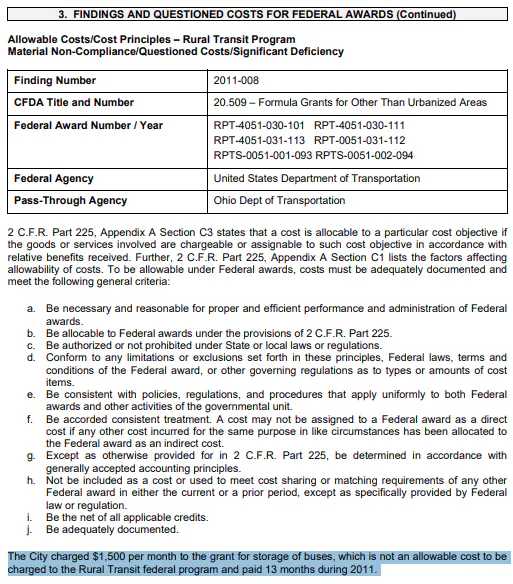

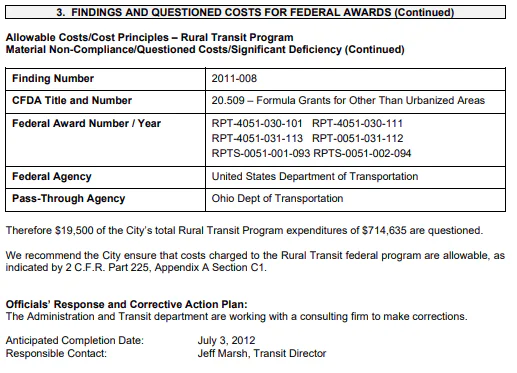

Finding 2010-016: Allowable Costs / Cost Principles — Rural Transit — Questioned Costs / Material Weakness (Federal)

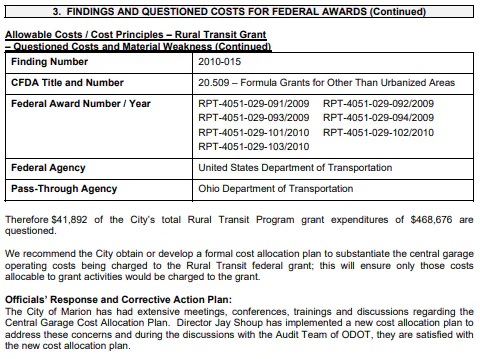

“$41,892 of the City’s total Rural Transit Program grant expenditures of $468,676 are questioned.”

Plain-Language Explanation. The City charged $1,500 per month in bus storage fees and a $75 per hour labor rate to the federal transit grant. ODOT had not approved these rates — the suggested labor rate was $58.67 per hour. The cost allocation plan included unallowable costs such as debt service for central garage construction. Total questioned costs: $41,892.

Forensic New World ERP IT Analysis. The General Ledger’s allocation functionality and the Project Accounting module include the capacity to be configured with approved cost rates for each federal grant. When a labor rate or indirect cost rate is entered that exceeds the grant-approved rate, the system rejects or flags the entry. Because these rate validation tables were not configured per the grant agreement, any cost at any rate could be charged to any grant without systemic challenge. The $75 vs. $58.67 rate discrepancy would have been caught automatically if the Project Accounting module had been configured with ODOT’s approved rate schedule.

Finding 2010-017: Expenditure Authorization — Rural Transit — Material Non-Compliance / Questioned Costs / Material Weakness (Federal)

“Per 2 C.F.R. Part 225 (OMB Circular A-87) requirements for time distribution for salaries.”

Plain-Language Explanation. Employees working on multiple federal and non-federal activities were not maintaining proper time distribution records as required by federal cost principles. Payroll certifications were not maintained. Without documented time distribution, the federal government has no assurance that the labor costs charged to the transit grant reflect actual time spent on grant activities.

Forensic New World ERP IT Analysis. OMB Circular A-87 requires employees who work on multiple cost objectives to maintain time distribution records — either semi-annual certifications (for employees working solely on a single cost objective) or monthly after-the-fact activity reports. New World’s Payroll/HR module includes the capacity to require activity codes for each pay period, linking hours worked to specific grants or cost objectives. Because this configuration was not utilized, payroll costs were allocated to grants based on estimates or fixed percentages rather than actual time worked — a violation of federal cost principles.

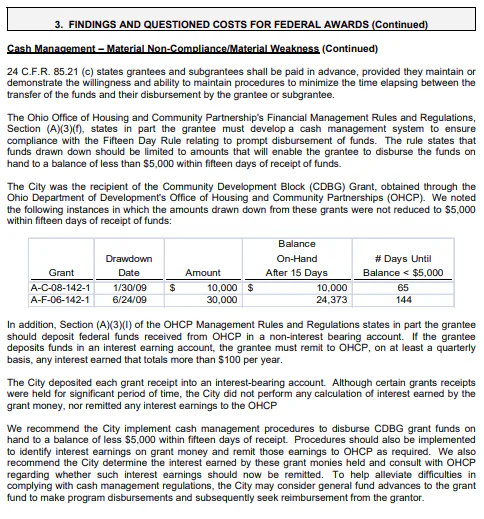

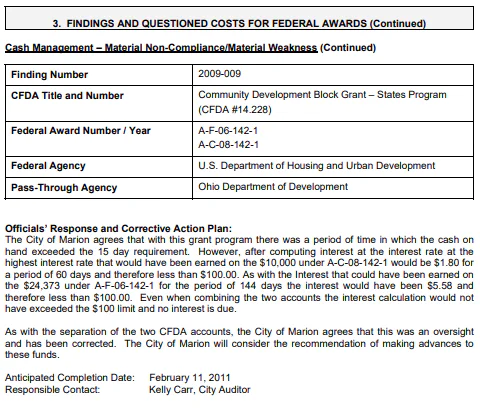

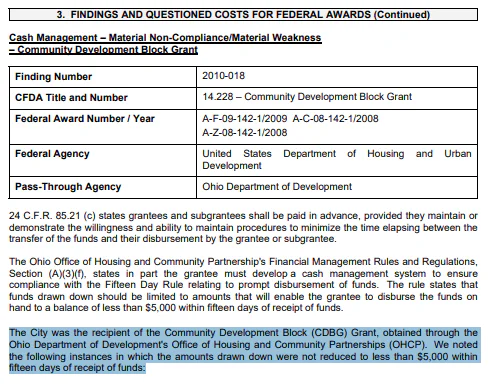

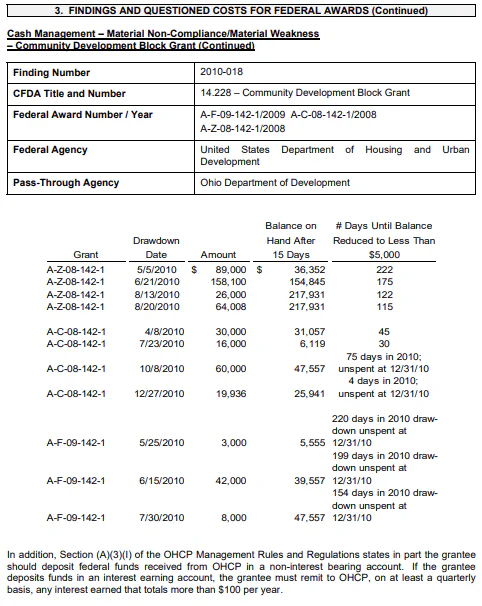

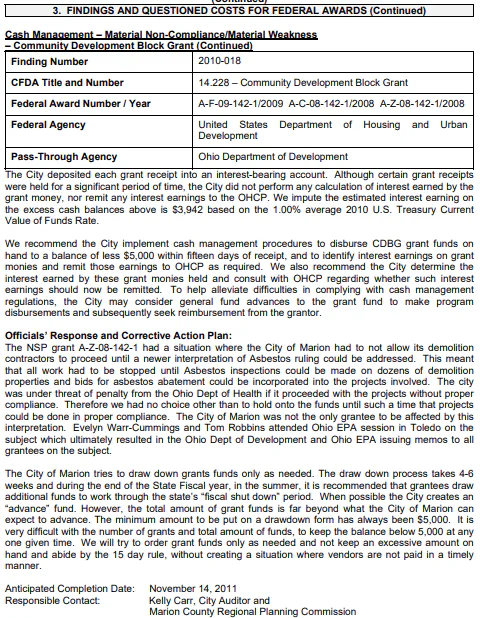

Finding 2010-018: Cash Management — CDBG — Material Non-Compliance (Federal)

Plain-Language Explanation. The City did not comply with federal cash management requirements for the CDBG program. Federal regulations require minimizing the time between receipt of federal funds and disbursement to avoid earning unauthorized interest on federal money.

Forensic New World ERP IT Analysis. The Cash Management module tracks the date of federal fund receipt and generates alerts when funds are held beyond the allowable period (typically 3 business days under the Cash Management Improvement Act). Because the Cash Management module was not configured to monitor these timelines, the City had no systematic way to monitor the timing of federal fund disbursement.

Finding 2010-019: Real Property Acquisition — CDBG — Material Non-Compliance (Federal)

Plain-Language Explanation. The City did not comply with federal requirements regarding real property acquisition and relocation assistance under the CDBG program. The Uniform Relocation Assistance and Real Property Acquisition Policies Act imposes specific documentation and procedural requirements on property acquisitions using federal funds.

Forensic New World ERP IT Analysis. CDBG real property transactions require specific compliance documentation that is tracked in the Grant Management or Project Accounting module. The system includes a compliance checklist and workflow for property acquisition transactions to ensure federally-mandated steps are followed. Because these features were not configured, the system did not flag CDBG expenditures coded to property acquisition object codes or require the necessary compliance documentation before processing.

Finding 2010-020: Expenditure Authorization — CDBG — Significant Deficiency (Federal)

“$13,365 in questioned costs resulted from CDBG expenditures exceeding budget, contrary to 24 C.F.R. 85.23.”

Plain-Language Explanation. CDBG expenditures exceeded the grant budget, generating $13,365 in questioned costs. The City was in contact with the Office of Housing and Community Partnerships throughout the audit process, but the overspending had already occurred.

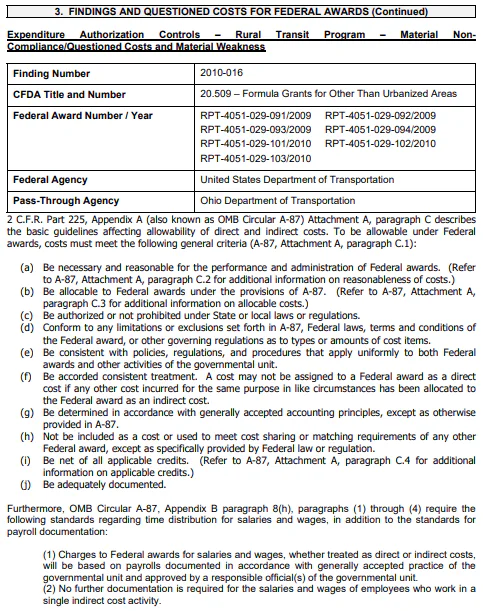

Forensic New World ERP IT Analysis. The same budget-checking override that allows City fund expenditures to exceed appropriations also applies to federal grant budgets when they are tracked in the General Ledger or Project Accounting module. New World’s budget-checking validation is designed to block overruns, such as the $13,365 identified, provided that override permissions are restricted to authorized personnel.

Because override permissions remained open to all users, grant budgets were as unprotected as City fund appropriations. The system’s functional capacity to enforce these limits was bypassed by the failure to configure restrictive user permissions.

Finding 2010-021: Allowable Costs / Cost Principles — CDBG — Material Non-Compliance (Federal)

Plain-Language Explanation. The City charged unallowable costs to the CDBG program, violating federal cost principles. Without a systematic process for validating which expenses are allowable under each federal grant, ineligible costs were charged to the grant.

Forensic New World ERP IT Analysis. The General Ledger and Project Accounting modules include the capacity to be configured with an allowable cost matrix for each federal grant, linking specific expense object codes to grant eligibility. The Purchasing module validates expense types against grant-specific allowable cost lists during purchase order entry to prevent ineligible charges.

Because this configuration step was not implemented, any expense code could be charged to any grant without systemic validation. This failure to utilize the system’s built-in cost-matching functionality allowed for the processing of expenditures without verifying their alignment with federal grant requirements.

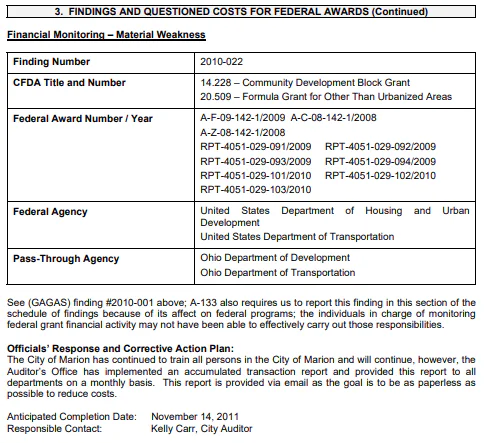

Finding 2010-022: Financial Monitoring — Material Weakness (Federal)

“We consider items 2010-012, 2010-014 through 2010-019, and 2010-022 to be material weaknesses in internal control over compliance.”

Plain-Language Explanation. This is the aggregate federal monitoring finding — eight individual findings classified as material weaknesses in internal control over federal compliance. The breadth of this finding demonstrates that the City’s federal program management was failing across every compliance dimension: financial reporting, cost allocation, cash management, property acquisition, and expenditure authorization.

Forensic New World ERP IT Analysis. This finding encompasses a systemic failure to configure the ERP for federal program compliance at any level. The Grant Management, Project Accounting, Cash Management, and Purchasing modules all possess features designed to enforce federal compliance, including:

- Grant-Specific Budgets: Automated ceilings to prevent over-expenditure.

- Approved Cost Rate Tables: Validation to ensure labor and indirect costs match agency-approved schedules.

- Cash Management Timing Controls: Alerts to ensure federal funds are disbursed within the allowable three-day window.

- Property Acquisition Checklists: Mandatory workflow steps to document compliance for real property transactions.

- Time Distribution Requirements: Mandatory activity codes to link payroll to specific cost objectives.

The aggregate nature of this finding — referencing eight other specific findings — establishes that none of these modules were configured for federal grant accounting. The ERP was deployed as a general municipal accounting system without utilizing the functional capabilities necessary to manage the City’s substantial federal program portfolio.

Audit Year 2011: Third Year, Same Failures — 11 Findings

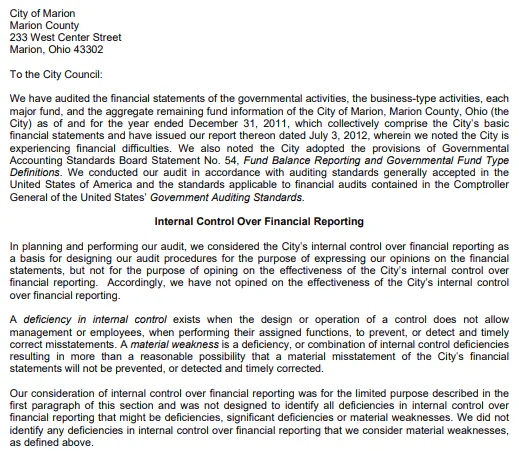

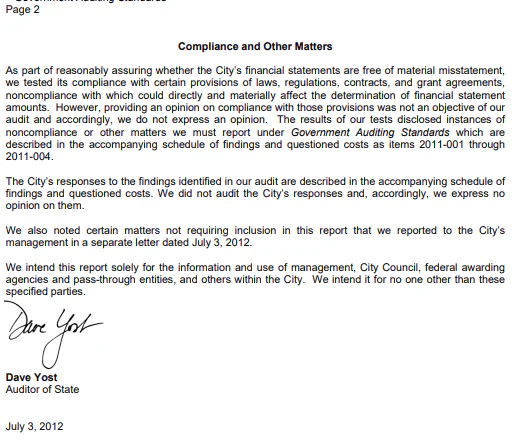

The Auditor of State’s audit for the year ended December 31, 2011 was filed July 3, 2012. It contained 11 findings — 4 GAGAS and 7 federal. The same categories repeated for a third consecutive year, and the Auditor noted the City had “suffered recurring losses from operations and has a net asset deficiency.”

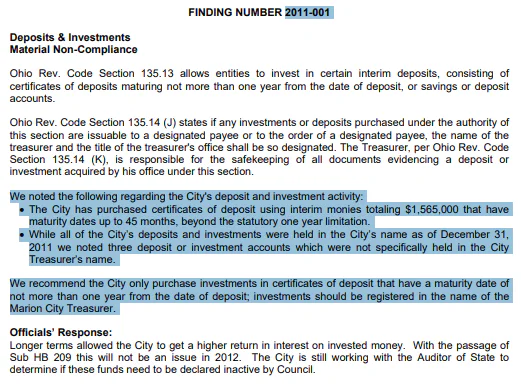

Finding 2011-001: Deposits & Investments — Material Non-Compliance

“Per Ohio Revised Code requirements for interim deposits and public depositories.”

Plain-Language Explanation. Third consecutive year of deposit and investment procedure failures. City Council still had not designated public depositories in compliance with Ohio law. A straightforward compliance step — meeting every five years to designate banks — remained undone year after year.

Forensic New World ERP IT Analysis. This is the third consecutive year that the Cash Management module’s investment tracking and compliance alerting features remained unconfigured.

New World is designed to automate oversight through scheduled reports and calendar notifications, which would have flagged the five-year depository designation requirement. The persistence of this finding over a three-year period establishes that no compliance tracking — manual or automated — was functioning, despite the system’s inherent functional capacity to manage these deadlines and monitor investment portfolios.

Finding 2011-002: Appropriations — Material Non-Compliance

“Contrary to Ohio Rev. Code 5705.36 and 5705.39.”

Plain-Language Explanation. Third consecutive year where appropriations exceeded estimated resources. The City continued to authorize more spending than it had revenue to support, in violation of Ohio law.

Forensic New World ERP IT Analysis. This is the third consecutive year that the Budgeting module’s validation against the County Budget Commission’s certificate of estimated resources remained unconfigured.

New World includes the functional capacity to enforce these legal ceilings automatically, preventing the City from exceeding its certified resources. The fact that this finding persisted for three consecutive years without systemic correction establishes that the City was treating audit findings as clerical responses rather than utilizing the ERP’s built-in controls to fix the underlying configuration gaps. This pattern demonstrates a continued reliance on manual oversight in an environment designed for automated compliance.

Finding 2011-003: Budgetary Expenditures Exceed Appropriations — Material Non-Compliance

“Expenditures may not exceed appropriations at the legal level of control.”

Plain-Language Explanation. Third consecutive year of expenditures exceeding appropriations at the object level. The budget-checking override permissions remained unrestricted. No corrective action had been taken on the Purchasing module’s security settings.

Forensic New World ERP IT Analysis. This is the third consecutive year that the Purchasing module’s budget-checking override permissions remained unrestricted. The system continued to allow any user with spending authority to bypass established budget ceilings.

At this point, a permanent operating pattern was established: the override was not a temporary transition-era issue, but a deliberate configuration. New World’s budget-checking feature was rendered effectively advisory-only because the restrictive permission settings—designed to enforce financial discipline—were not utilized. By allowing universal override access, the City bypassed the system’s functional capacity to prevent unauthorized expenditures and maintain budgetary control.

Finding 2011-004: Negative Fund Balances — Material Non-Compliance

“The existence of a deficit fund balance is an indication that monies from one fund were used to pay the obligations of another fund.”

Plain-Language Explanation. Second consecutive year of negative fund balances. Multiple funds ended 2011 with deficit cash balances, meaning money from other funds was used to cover their obligations. The Auditor added a critical observation: the City had “suffered recurring losses from operations and has a net asset deficiency” — meaning the City’s total liabilities exceeded its total assets. Marion was, in accounting terms, insolvent.

Forensic New World ERP IT Analysis. The General Ledger’s fund balance controls remained unconfigured, and no hard-stop existed for transactions that would drive fund balances into the negative. Because the system’s negative-balance validation was not utilized, cross-fund subsidization continued without the oversight of systemic controls.

The “net asset deficiency” finding is significant from an ERP perspective: it establishes that the cumulative effect of uncorrected, system-enabled errors—including misallocated income tax, uncontrolled spending, and unauthorized cross-fund payments—eroded the City’s financial position to the point of technical insolvency. New World is designed to enforce fund integrity by blocking deficit-causing transactions and flagging interfund activity for authorization; however, by leaving these functional capacities inactive, the City allowed the system to process a volume of errors that eventually compromised its overall financial stability.

Finding 2011-005: Filing of Single Audit — Material Non-Compliance (Federal)

“The City expended $2,033,680 in federal awards in 2010. Because timely financial statements were not prepared, the 2010 Single Audit report filing was not completed by the deadline.”

Plain-Language Explanation. Second consecutive year of late Single Audit filing. The City’s federal award expenditures had increased to over $2 million, making timely compliance reporting even more critical. The City responded: “This has been corrected for 2012 and will not apply next year.”

Forensic New World ERP IT Analysis. The ERP’s inability to produce timely, reconciled financial data continued to cascade into late federal filings. New World includes automated year-end close procedures and GAAP conversion tools designed to streamline the transition from budgetary tracking to financial reporting.

Because the General Ledger was not configured to utilize these automated workflows, the delay became structural. This was a system capability problem rather than a staffing issue; without the proper configuration of the General Ledger’s closing modules, the system could not generate the accurate, reconciled data required for timely federal filings. The failure to implement these built-in reporting features forced a reliance on manual reconciliation, which consistently lagged behind federal compliance deadlines.

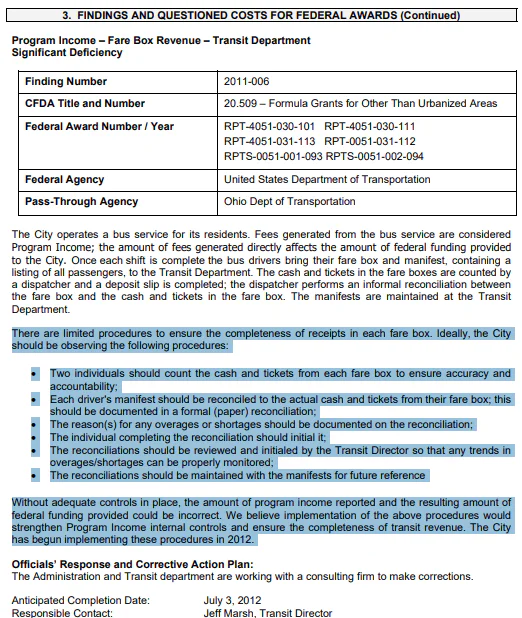

Finding 2011-006: Program Income — Fare Box Revenue — Transit — Significant Deficiency (Federal)

“There are limited procedures to ensure the completeness of receipts in each fare box.”

Plain-Language Explanation. Third audit cycle documenting the same fare box revenue control deficiency. Passenger fares are classified as Program Income under FTA regulations, meaning the amount directly affects federal funding calculations. The City stated it was working with a consulting firm to improve procedures, but the finding persisted.

Forensic New World ERP IT Analysis. This is the third consecutive year that the Cash Receipting module remained unconfigured for transit fare box reconciliation. The engagement of an external consulting firm suggests the City recognized the issue as systemic; however, they sought external intervention rather than utilizing the configuration options already available within the ERP.

The necessary solution—dual-entry cash receipting with manifest reconciliation and a supervisor approval workflow—is a core functional capacity of New World. When properly configured, the system requires an independent count of physical cash and a separate entry of the driver’s manifest, automatically flagging variances for management review. Because these built-in internal controls were not implemented, the transit department continued to operate with a high risk of revenue loss and insufficient financial oversight.

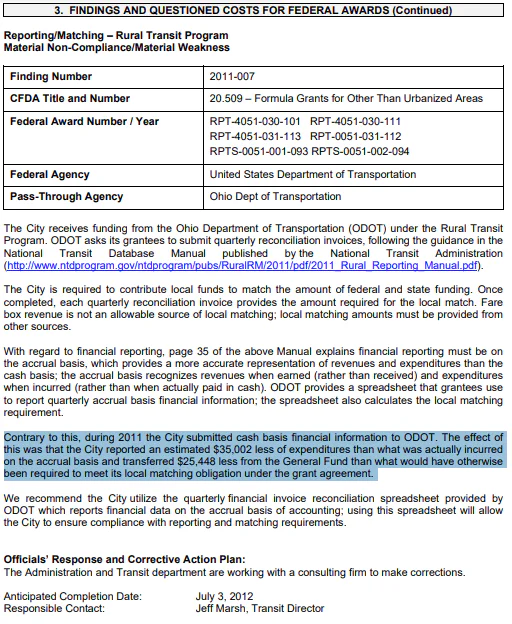

Finding 2011-007: Reporting/Matching — Rural Transit Program — Material Non-Compliance / Material Weakness (Federal)

“During 2011 the City submitted cash basis financial information to ODOT” contrary to required accrual basis.

Plain-Language Explanation. Second year of submitting cash-basis reports to ODOT when accrual-basis was required. The City understated expenditures by $35,002 and transferred $3,779 more from the General Fund than required for the local match. The City was again working with a consulting firm.

Forensic New World ERP IT Analysis. The General Ledger’s fund configuration for the Rural Transit Program remained restricted to cash-basis accounting. As a result, the system continued to produce cash-basis reports that were submitted to ODOT without the necessary accrual adjustments for federal compliance.

New World’s Grant Management module includes the functional capacity to maintain the specific reporting basis requirement for each grant—whether cash, accrual, or modified accrual—and generate financial reports accordingly. Because this configuration was never established, the system could not automate the conversion of transit data into the format required by state and federal agencies. This failure to utilize the module’s reporting basis settings forced the City to rely on a fund structure that was fundamentally mismatched with its grant reporting obligations.