With the city of Marion currently considering the elimination of the 100% income tax credit provided to city residents who work elsewhere and pay income taxes to another municipality, now is a good time to share the story of how Marion came to have an income tax.

Prior to the 1st of June 1959, if you worked or operated a business in the city of Marion, you didn’t pay any of your earnings to the city in the form of a municipal income tax.

The much-smaller-than-today local government, which administered an economically vibrant and prosperous city with a population of about 37,000 (larger than today’s Marion which has a population of about 35,000), operated with a general fund budget of $751,952, which is equal to $8,436,901 in today’s money according to the US Bureau of Labor Statistics’ CPI Inflation Calculator, and a total budget of $2,309,952, which is equivalent to $25,917,661 today.

Just to put that in perspective, last year, the general fund budget for the city of Marion was $18,725,200. Adjusted for inflation, that’s an increase of 121.94% from 1959! And with a smaller population!

And the total city budget in 2025 came in at a whopping $71,699,881!!! An inflation adjusted increase of 176.65% since 1959!!!

As far as revenues in 1959–in the days before the income tax–city government was largely funded by property taxes (35.05%), as well as sales taxes (8.16%), license fees, permit fees, fines, parking meter fees, etc.

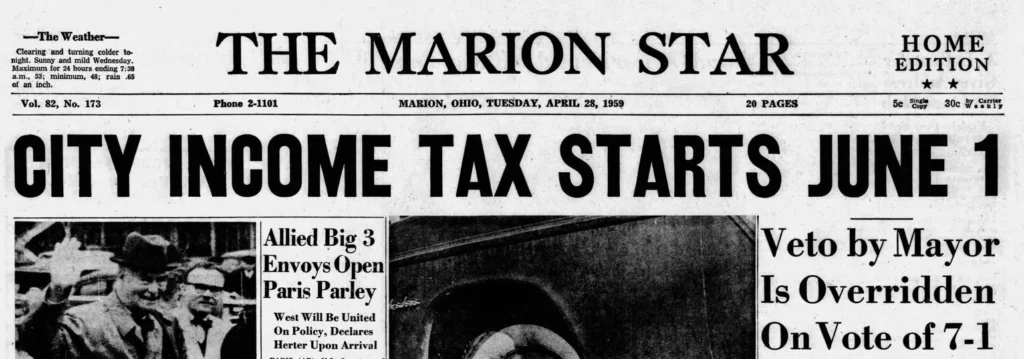

But that all changed on the 1st of June 1959.

The story leading up to the city’s implementation of an income tax is an interesting one.

It had been discussed a few years prior, but the powerful private sector labor unions in town were largely opposed to the idea, so it didn’t get anywhere.

They were won over by 1958, with alleged promises of work contracts for private sector union workers and pay increases to public sector union city employees.

On the 26th of March, Council passed an ordinance establishing a 0.6% income tax on all earned income. The vote was 7-2 with the only dissents coming from Lowell Doyle (R-3rd Ward) (1928-2010) and Norma Jacob (D-5th Ward) (1923-2025).

The tax was promised to expire after 1.5 years, and the proceeds were to be used for street and sewer projects only.

Skeptical and unconvinced by the promises, Mayor Wendell L Strong (R) (1922-1987) vetoed the measure.

Undeterred by Mayor Strong’s strong response, Council overrode his veto by a vote of 7-1, with Doyle the only nay vote. Jacob abstained that go-around, likely because her husband, George T Jacob (1914-1989) was in the process of organizing a ballot initiative against the tax.

The income tax did indeed go into effect on the 1st of June; however, on the 26th of June, George Jacob and a group of citizens filed the necessary paperwork to seek a repeal of the tax by the citizens of Marion in the upcoming November election.

The labor unions and city workers rallied to keep the tax and engaged in a fairly large-scale and presumably well-funded campaign in its support.

The ballot language was also a little bit confusing as voters had to vote “No” to keep the tax and, conversely, they had to vote “Yes” to repeal it.

Whether it was confusing or not, the repeal initiative was soundly defeated by a vote of 7,299 to 3,409.

The income tax naysayers were proven right, though, as much of the funds ended up in the city’s general fund.

Additionally, the income tax did not go away a year-and-a-half later. It was repeatedly renewed and gradually increased to its present 2% rate–and all the while the size and scope of government have grown along with it.

Today, municipal income taxes are the primary source of revenue for the city of Marion, representing over half of the city’s annual receipt of funds.