Over the past two decades, the Marion City School District has navigated a rocky financial path. From being placed under state “Fiscal Watch” in 2004 to facing a looming multi-million dollar deficit today, the numbers tell a story of questionable priorities and unchecked spending.

Recently, in an attempt to justify the district’s current financial nosedive, a new narrative has emerged in the public network.

Defenses have been circulating and suggest that the district was forced into this deficit because it had to “purchase entirely new curriculum for nearly every subject,” “replace outdated technology that had not been cycled out over the previous decade,” and enact massive salary hikes because teachers supposedly “went without a base pay increase for eight years.”

Here at Marion Watch Investigates, our team pulled the actual state audits, financial records, and the district’s own internal information along with recent reporting by Swamp Fox.

We put all of our resources into looking closer at the situation.

Not only is the defensive rhetoric factually false, but using these excuses to justify the current financial crisis actually exposes a much deeper level of systemic issues.

Because we have pulled all audits and other documentation as far back as 1999, we may go deeper at a later time, add further information, and zero in on the situation surgically.

But for now, this focused article will provide the essentials.

Dismantling the Fiscal Narratives

Myth 1: A “Decade” of Outdated Technology The claim that the district’s technology had not been cycled out over the previous decade requires the taxpayers to suffer from collective amnesia.

During the COVID-19 pandemic, school districts across Ohio were flooded with millions of dollars in federal ESSER relief funds, specifically earmarked for one-to-one devices, digital infrastructure, and curriculum.

The district’s own 2024 Single Audit provides the smoking gun. [Source: Marion City School District 2024 Single Audit, Schedule of Expenditures of Federal Awards, PDF Page 95].

According to this official state document, the Marion City School District spent a staggering $9.29 million in Education Stabilization Funds (CARES/ARP) in 2024 alone. To suggest the district was forced into a deficit because it inherited a “decade” of untouched, outdated tech ignores the millions in federal pandemic relief that just flowed through their accounts.

Myth 2: The “All-At-Once” Curriculum Buy Standard public school financial management dictates a staggered curriculum adoption cycle (e.g., buying new Math curriculum one year, English the next). If the district actually chose to purchase “entirely new curriculum for nearly every subject” all at once out of their general fund, that shouldn’t be used as a defense. That is an admission of catastrophic financial planning and an irresponsible drain on the budget.

Furthermore, the district’s own financials disprove that this is what drained the budget.

According to the data, only a microscopic 2.19% of the general fund was actually spent on “Materials & Supplies” (which includes curriculum), while nearly 30% was poured into outside “Purchased Services.”

Myth 3: The “Eight-Year” Pay Freeze The narrative claims teachers went a staggering eight years without a base pay increase prior to 2023. Public records filed with the state completely destroy this claim. [Source: State Employment Relations Board (SERB) Public Database – Marion Education Association Collective Bargaining Agreements]. Official, legally binding union contracts were signed and went into effect in 2015, 2019, and 2022, all of which included structured base salary schedules and routine step increases. The claim of an eight-year freeze is a manufactured fiction designed to make the district’s massive spending hikes look like a necessary “catch-up” rather than what they actually are: budget bloat.

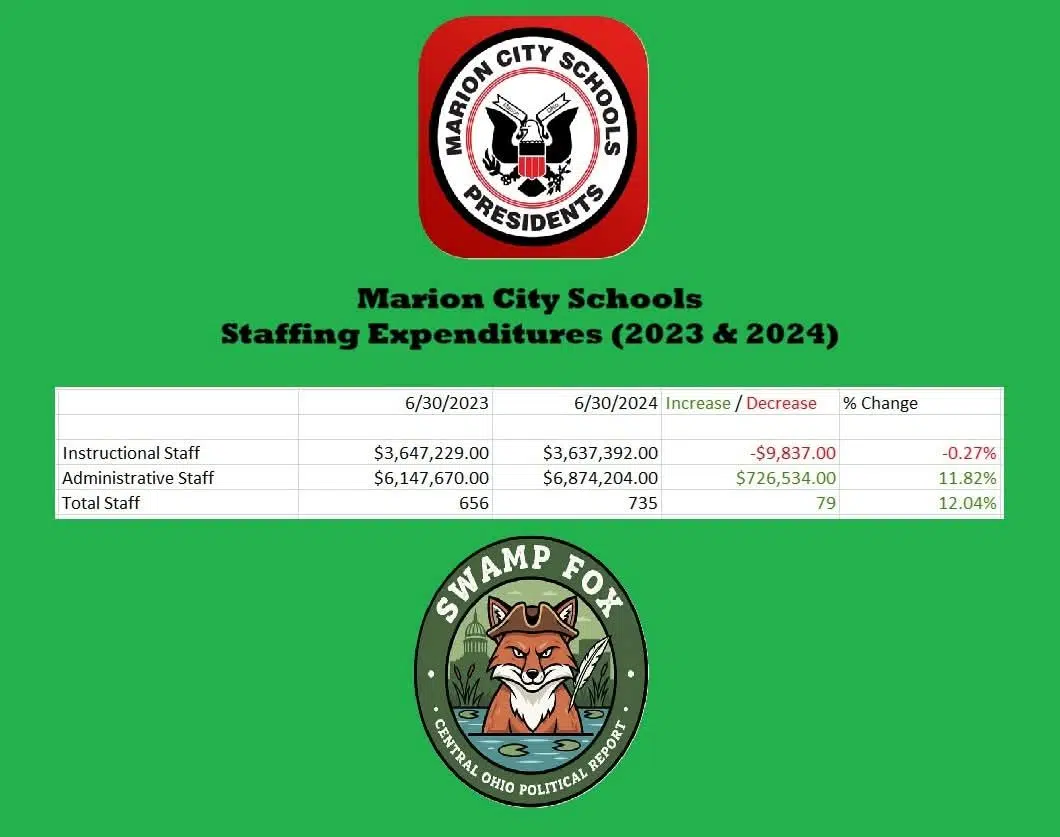

The Real Driver: 79 New Hires and a $10 Million Jump

With that flimsy rhetoric out of the way, we can look at the real math. As Swamp Fox recently reported, the 2026 projected budget has a deficit of exactly $3,905,095—and the projections for 2027 through 2029 only get worse.

How did they get here? Overall budget expenditures have increased by over $11 million since 2023, while revenues only went up by a little over $3.2 million. Swamp Fox’s investigation into the state audits revealed exactly where that money went:

- A Massive Hiring Spree: Between 2023 and 2024, the district increased its staffing by 79 employees (jumping from 656 to 735). That is an astronomical 12.04% increase in headcount in a single year.

- Exploding Compensation: The district will spend over $10 million more on salaries and benefits in 2026 than it did in 2023.

As Swamp Fox highlighted, during a board meeting on October 20, 2025, Treasurer Jolene Carter made it clear that the district’s deficit projections were known to the Board of Education before they decided to hand out those massive pay increases in 2025.

The Salary Disconnect: Underpaid Teachers, Overpaid Administrators?

While the district’s total compensation costs surged by $10 million, official state comparison graphics reveal a glaring disconnect in exactly who is benefiting from that cash.

The average teacher in Marion City Schools makes $63,618—falling short of both similar districts ($65,581) and the state average ($70,305).

However, when you look at the top of the food chain, the script flips entirely.

The average administrator in Marion pulls in $91,959—beating both similar districts ($90,733) and the state average ($89,335).

This proves that the massive surge in payroll isn’t just about catching up “frozen” teacher salaries. The district is actively choosing to underpay the educators standing in the classrooms while overpaying the administrators sitting in the offices.

Where Else is the Money Going? The Outsourcing Anomaly

With an extra 79 employees on the payroll, you would assume the district is handling all of its operations in-house. You would be wrong.

A dive into the district’s own FY 2024 “General Fund Operating Expenditures” reveals a massive anomaly in how the budget is being consumed.

While the vast majority of any school’s budget is rightfully swallowed by personnel costs, Marion City Schools is actively pouring a staggering 29.56% of its General Fund into “Purchased Services.”

In school finance, “Purchased Services” is the accounting line used for outside contractors, external consultants, outsourced labor, legal fees, and third-party vendors. For a district to hire nearly 80 new employees, yet still bleed roughly 30% of its operating budget into outside contractors—while spending a microscopic 2.19% on actual “Materials & Supplies”—points to severe administrative bloat and unchecked discretionary spending.

The Accounting Problem: A Refusal to be Transparent?

Why is it so hard for the public to easily see the true weight of these financial decisions?

It comes down to how the district keeps its books. Ohio Administrative Code § 117-2-03(B) legally requires school districts to use a standard reporting system called GAAP (Generally Accepted Accounting Principles). GAAP provides a fully transparent picture of long-term debts, assets, and future pension liabilities.

Instead, the Marion City School District intentionally violates this state code, using a simple “cash basis” method that hides the true weight of their long-term financial commitments. Because of this, independent auditors hit the district with a severe “Material Non-Compliance Finding” every single year.

- 2016 (Finding 2016-001)

- 2017 (Finding 2017-001)

- 2018 (Finding 2018-001)

- 2019 (Finding 2019-001)

- 2020 (Finding 2020-001)

- 2021 (Finding 2021-001)

- 2022 (Finding 2022-001)

- 2023 (Finding 2023-001)

- 2024 (Finding 2024-001)

Prior to 2016 (such as in the 2014 and 2015 audit documents), the independent auditors noted that the district’s financial statements were presented in accordance with GAAP.

The shift occurred during the 2016 fiscal year when the district officially decided to transition to a modified cash basis, citing a desire to “reduce time and costs” in their Corrective Action Plans, which triggered this recurring statutory violation.

What is the district’s excuse for violating state transparency codes? In the official Corrective Action Plan filed in the 2024 audit, the district’s Treasurer explicitly states they refuse to convert to GAAP “in order to reduce time and costs.”

The 2012 “Scrubbing” Scandal

If you want to understand the community’s deep distrust of financial narratives, you have to look at the district’s track record with data. In 2012, the state launched an investigation into attendance “scrubbing”—a practice where districts improperly withdraw underperforming students to make their state report card scores look better. Marion City School District was explicitly named by the Auditor of State as one of the exact five districts in Ohio found to have improperly withdrawn students. While the Ohio Department of Education eventually cleared the district of malicious, license-revoking intent two years later in 2014, the initial state audit’s findings of improper data manipulation cast a long, justifiable shadow over the district’s current financial excuses.

The Bottom Line

The Marion City School District is driving straight toward a financial wall of its own making. The community cannot rely on rhetoric blaming a “decade of neglect” when their own audits show $9.2 million in federal stabilization spending in 2024 alone, and state records prove a history of routine union negotiations.

By their own admission, they are on a trajectory to wipe out $26 million in cash reserves by 2029. As Swamp Fox noted, unless the school district starts being good stewards of the taxpayer’s money and goes back to the fundamentals of education by reining in their top-heavy paychecks and massive purchased service expenditures, they will inevitably be forced to ask the taxpayers of Marion to bail them out.

Works Cited (Click Here)

Works Cited & Source Material

Primary Audits & Government Documents

Auditor Reports Full Directory (1999-Most Recently Available):

https://drive.google.com/drive/folders/1Meai6VMA4A0M91CKnIoe362646jsuE5K?usp=drive_link

Primary Audits & Government Documents

- Charles E. Harris & Associates, Inc. (2024). Marion City School District Single Audit For the Year Ended June 30, 2024. Prepared for the Ohio Auditor of State. (Contains the official “Material Non-Compliance Finding 2024-001” for refusing GAAP accounting to “reduce time and costs,” and the Schedule of Expenditures of Federal Awards proving $9.29 million in federal stabilization spending in 2024).

- Auditor of State Dave Yost (2012). Marion City School District Performance Audit. Columbus, OH: Ohio Auditor of State.

- Auditor of State Betty Montgomery (2004). Declaration of Fiscal Watch: Marion City School District. Columbus, OH.

District Internal Records

- Marion City School District (2024). Five-Year Forecast and General Fund Operating Expenditures. Official internal district graphics. (Provides the mathematical proof of the cash balance plunging by 2029, money spent on Purchased Services).

- State of Ohio District Profile Reports. Marion City School District Average Salary Comparisons. Official district-provided graphics. (Validates the $63,618 average teacher salary vs. the $91,959 average administrator salary).

External Public Records & Reporting

- Local Meeting Minutes / Public Record (October 20, 2025). Marion Board of Education Meeting. (Validates the board’s public discussion attributing the deficit to the loss of ESSER funds and rising personnel costs prior to approving pay raises).

- State Employment Relations Board (SERB), State of Ohio. Negotiation Documents between the Marion Education Association and the Marion City Board of Education. (Publicly filed Collective Bargaining Agreements effective 2015, 2019, and 2022).

- Ohio Auditor of State Archives (October 23, 2012). “No Evidence of Scrubbing Found in Second Phase of Attendance Data Audit” / Initial 2012 Scrubbing Release. Columbus, OH.